Winter is always a tricky time for buyers – expert commentary is seemingly everywhere detailing why next year will be a crisis, with market participants often using selectively pessimistic views to support their own agenda/to bring about a self-fulfilling prophecy?

Let’s face it, traders/speculators need markets to move – big price swings mean big profits, regardless of the direction of travel.

This winter (like every winter before it) is no different – with the onset of inevitably less benign conditions (cold, still weather/ increased gas-for-power burn/storage withdrawal), all eyes turn away from the geopolitical turmoil that had (ostensibly) been moving markets over Summer-24, and instead focus on speculative noise about next year’s gas storage targets.

Not surprisingly, market participants respond with fear and avarice – arguably, the two emotions primarily responsible for ALL financial market movements (equities/indices/FOREX/bonds/commodities etc).

We’ve heard a lot this week about concern over how Europe will fill its storage fullness to the “required” 90% levels by Nov-25 – right now, European inventories sit at 85%, lower at this point than in 3 of the last 5 years (though, hysteria aside, levels are still above the average for the last 8 years).

So is it too early to be sounding the alarm?

Is it not the case that prices are just wintry?

Well, with Europe’s storage levels continuing to diminish as we approach the height of the heating season, both near- and far-term gas contracts are inevitably trading higher to reflect increased scarcity – but isn’t this just good old fashioned supply/demand dynamics at work?

Today, in fact, the UK system opened healthy and long this morning (supply outstripping demand forecast) amid strong LNG nominations and steady Norwegian/UKCS flows – total demand is below seasonal norms and temperatures are around 4°C above seasonal norms.

So, let’s look in more detail at why some market participants are seemingly getting behind the belief that we should be already panicking over next winter’s storage levels.

Well, the well-publicised end of the Ukraine/Russia transit deal and the (to be expected) depletion of stored gas during the recent cold spell has prompted the International Energy Agency (IEA) to warn that Europe may be facing a “new energy crisis” (IF we have very cold winter).

Though, let’s not forget, IF we have a cold winter in any year, it will impact on storage pressures in the subsequent summer – there’s nothing “new” or revelatory about it.

One could fairly argue the IEA is hedging its bets and prophesying the doom which lies ahead safe in the knowledge that if it doesn’t happen, everybody will be so relieved they’ll not care what the IEA spouted months previous – or if it does come to pass, the IEA can say it told us so.

Don’t get us wrong, we do face new pressures this year amid the ongoing supply tightness/over-reliance on LNG caused by the loss of Russia’s gas, and the ongoing conflict.

With a total volume of over 30 bcms, Ukraine enjoys the largest storage capability in Europe – ordinarily, a further 15 bcm are made accessible for use by European partners.

In fact, last year foreign speculative traders kept over 3.2 bcms in Ukrainian tanks over the winter, but they’ve chosen to stay away this year due to Russian strikes on Ukraine’s energy infrastructure.

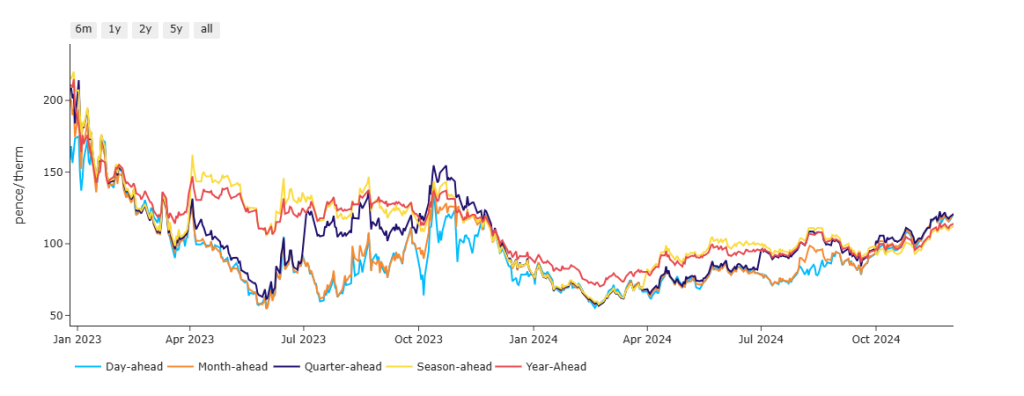

Traditionally of course, gas tends to be cheaper in the summer when demand is lower – in addition, it’s normal in the summer months for very short-term delivery (Day/Month-Ahead) to diverge from Season/Year-Ahead to reflect summery conditions (see chart below showing just this, as well as how Day/Month/Qrtr/Season/Year-Ahead prices ordinarily return to near-parity over winters when prices get “tighter”).

Anyway, historically traders buy in the warmer months with a view to storing gas to sell at a profit during the winter peak heating season.

However, very unusually, gas for delivery in Summer-25 is now being priced at a premium to Winter-25.

And so, this unusual development surely reflects the fear (not fact) that Europe will need to draw heavily on its gas storage over the coming winter months, and will then struggle to replenish inventories in the summer months – and so summer gas will be scarce, hence the premium.

However, with weather forecasts for the coming weeks flip-flopping on a daily basis, it’s important not to get swept away too much by the fervour – remember, markets have a tendency to fall twice as quickly as they rise.

If traders are “long” (have a buy position) for any respective period of delivery, then of course they’re going to support any news which takes that market higher (so they can sell at at a profit).

For the time being, all buyers can do is keep one eye on the facts, and the other eye on the rife speculation – whilst nobody has a crystal ball, it’s true to say that UK Summer-25 gas is only at a 3p/therm (0.1p/kwh) premium to Winter-25 at the time of writing!

And the premium is all in Q2, not Q3.

It’s worth considering as well, that China may come to Europe’s aid.

Whilst it’s true that Asian LNG demand ordinarily poses a risk for Europe (by increasing competition for cargoes), remember that countries across Asia are not willing to buy LNG at any price.

Why would they when they have other (granted, less sustainable) options – like coal and oil?

Notably, China’s LNG imports have fallen Y-o-Y to November (as have India’s) – whilst Europe’s are on the up, which could be a reflection that China is happy for Europe to pay the premium whilst it falls back on plentiful (and cheaper) coal reserves.

Objectively, it may be, of course, that for some buyers taking a wait-and-see approach will give them too many sleepless nights between now and next summer – as such, it’s worth pointing out that the value on offer for delivery Summer-25/Winter-25 is still better than that which was being offered for the same periods of delivery between Apr-22 to Jan-23 – so comparative value still remains.

So far this month, Monthly Day-Ahead averages are on target to achieve 115.4p/therm (or approx. 3.938p/kwh excluding non-gas).

ELECTRICITY & CARBON

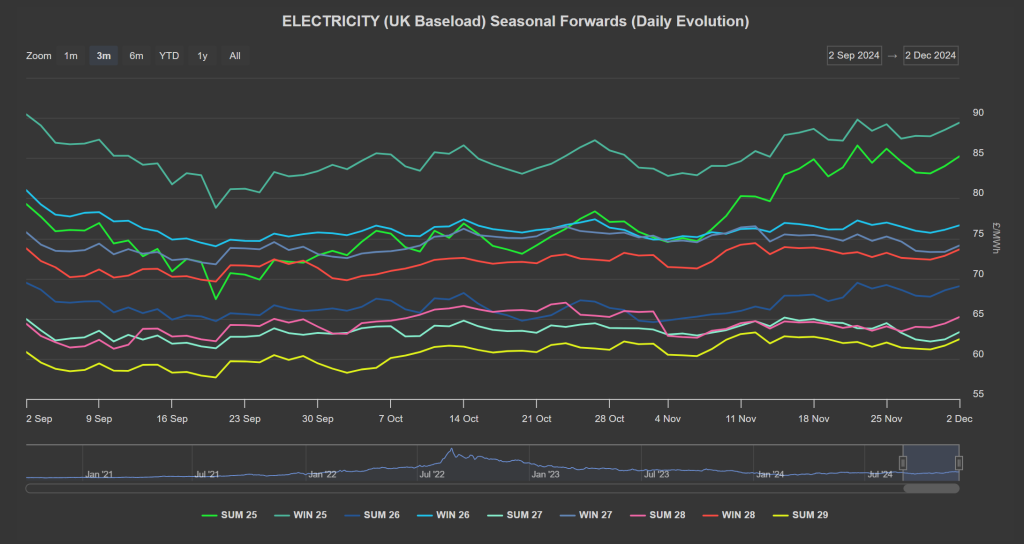

To clarify, UK electricity is not suffering from the same condition as UK gas i.e., Summer-25 is NOT at a premium to Winter-25 (see below chart).

Looking to the continent for direction, it’s cold and getting colder – thankfully, the outlook has revised windier for the short-term with a strong ramp-up expected on Wednesday PM in the UK, and Thursday across Germany.

Low to modest levels of solar generation are forecast across CWE (Central Western Europe) this week.

Modest precipitation is forecast today over the Alps and the Pyrénées amid moderate snowfalls due to the zero-degree level standing below 2kms high – so fairly flat run-of-river.

On the Carbon markets, EUAs (European) prices opened bullish yesterday (mirroring gas prices) off the back of the news that the European Commission lowered the gas storage target from to 50% from 45% for February.

The Dec ’24 benchmark contract reached a high of €70.14/tn with the auction clearing at €69.4/tn – the day closed at €68.83/tn (+0.63%) – so little movement, noise aside.

It clearly underperformed benchmark European gas (TTF closed up 1.77%).

With European temperatures expected to drop in the coming days, weekly electricity contracts closed higher yesterday with demand likely to rise.

Back in the UK, UKA mid-price rose to £37.08/tn off the back of Compliance buyers bargain hunting at last week’s low levels (£35.56/tn last Wednesday).

The UK’s electricity generation mix is bullish in nature today with renewables contributing 15%, thermal at 56% (gas and coal) and low carbon at 15% (nuclear and imports).

Monthly Day-Ahead averages for the month so far are on target to achieve £106.008/mwh (or 10.6p/kwh excluding non-energy).