Noise aside (of which there’s plenty), market movements are what you’d expect for the time of year.

Near-term delivery prices have continued to soften in keeping with summer conditioning, reflecting lower risk-premium amid increasingly comfortable fundamentals (low demand, solid supply, lower withdrawals, increasing injections).

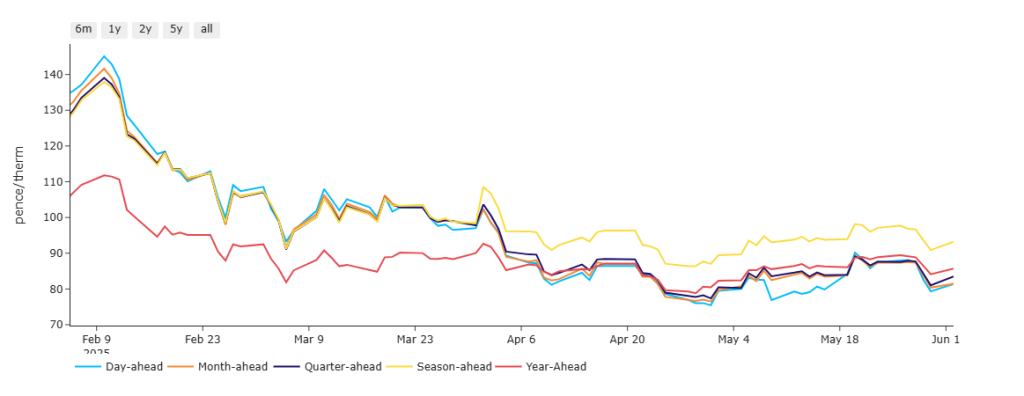

Please see chart below detailing Day-Ahead selling at a premium to all other periods of delivery back in Feb-25, only then to fall to posting a discount to all other periods of delivery beginning Summer-25 (1st Apr).

Forward prices (for periods of delivery further out) continue to find support against a backdrop of geopolitical impacts (which, in turn of course, influence supply dynamics).

The traditional summer maintenance season is well underway, with Norwegian flows operating some way below capacity – limiting supply, and putting more pressure on LNG arrivals to Europe.

68% of Europe’s LNG imports in April came from the US – however, due to a combination of scheduled/unscheduled outages, US LNG exports to Europe fell in May whilst also increasing slightly to Asia (off the back of marginally increased Asian cooling demand).

Nonetheless, US LNG netbacks still favour Europe as a more profitable destination for LNG vessels (another reason why prices look destined to remain supported for the rest of summer, to ensure LNG continues to arrive at our shores with a view to achieving sufficent storage in time for the heating season beginning Oct-25).

Other supportive key drivers include the Ukraine conflict and the US-China trade standoff.

With yet another round of failed ceasefire talks yesterday (amid ongoing drone attacks from both sides), an end to hostilities seems all too distant – as do the resumption of Russian gas flows.

Bizarrely, worsening US-China relations would likely be bearish for the wider energy complex – as Chinese demand would invetiably fall amid worsening production outputs, and more LNG would be made available to Europe (at reduced competition) – but for now the standoff is contributing to volatility.

So, whilst prices have softened significantly versus Feb/Mar-25, we’re reaching a stage in the summer where it’s difficult to see how prices will fall further (despite lower demand and increasing storage levels).

European storage is now at 48% versus the 5-year average of 56% – so any cause for alarm has surely abated.

On the trading side, clients running flexible capability are increasingly picking up significant volumes of the attractive Forward Summer prices currently on offer.

It would seem prudent for buyers to continue to scale-in modest hedges over the coming days/weeks whilst the going is good.

This month’s UK gas Day-Ahead averages are holding steady at 81p/therm (or approx. 2.8p/kwh excluding non-gas).

ELECTRICITY & CARBON

Mirroring the gas markets, please see chart below detailing electricity Day-Ahead selling at a premium to all other periods of delivery back in Feb-25, only then to fall to posting a discount to all other periods of delivery beginning Summer-25 (1st Apr) – as such, clients floating on the Day-Ahead across the summer months remain in good shape.

Electricity prices down the curve remain tethered to gas movements.

Winter-25 is having another go at breaking below £85/mwh at the time of writing (though still someway above the £80/mwh lows printed on 1st May).

On the Carbon side of things, markets are flat and consolidating in a tight range just above £50/tn on the mid-price.

Today’s UK electricity generation mix is very bearish (and ‘summery’) in nature reflecting warm and windy conditions – specifically, renewables are contributing 66%, thermal at 11% (gas and coal) and low carbon at 20% (nuclear and imports).

So far this month, electricity Day-Ahead averages have dropped off due to a reduction in gas-for-power burn over the last week or so – currently very low at £39/mwh (or approx. 3.9p/kwh excluding non-energy).

On the trading side, clients running flexible capability are encouraged to scale-in modest hedges over the coming days/weeks whilst markets still offer solid comparative value.