The week started on a bullish note yesterday off the back of reduced Norwegian flows due to a crack in a pipeline on the Sliepner platform.

Norwegian export was cut to 256 million cubic metres (mcm) versus the expected 300 mcm.

The unscheduled outage (and associated fears of supply tightness) spooked market participants, causing a short-lived bullish rally that gave back all of its gains by the end of the day.

Langeled pipeline flows were indeed at zero this morning, and likely will remain so until the crack is repaired (reportedly by Friday).

Whatever the duration of the outage, it’s important to keep this bump in the road in perspective.

Lest we forget, MRS (European storage) remains comfortable – at 70% versus the 5-year average of 57%.

Looking at the bigger picture, a reduction in Norwegian flows could be replaced by an increasingly flexible LNG market.

Whilst increased Asian demand is supportive of prices, China is not ready to import LNG at any price.

If prices were to remain permanently high, China would likley reduce its LNG (and coal) imports by increasing domestic coal production.

Despite yesterday’s bullish tone, the UK system was long this morning (supply outstripping demand forecast).

Norwegian nominations to Europe have been stable today despite the ongoing outages (with several expected to end tomorrow, and with improving capacity as we approach the weekend).

On the demand side, the outlook is neutral to bearish against a backdrop of continually improving weather forecasts as we head deeper into summer conditions.

Geopolitically, markets are firmly supported by fears that Russia will further reduce gas exports into Europe (should arbitration claims against Gazprom result in a recent court ruling being enforced).

The issue, whilst unresolved, will remain supportive (with the feared outcome being Gazprom ceasing to deliver gas to several Central European countries).

As detailed in previous reports, markets have risen steadily since the onset of Summer-24 (beginning April).

However, 119 days of Summer-24 remain (with 65 days now used up) – so we’ve got the best part of two thirds of Summer-24 still to come.

Whilst it’s conceivable we’ve already seen the bottom of summer pricing, it’s not panic stations just yet.

Scaling-in, so as to mitigate loss of summer value, is increasingly the consensus approach amongst clients (with open volumes at the front Seasons – Winter-24/Summer-25/Winter-25).

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24).

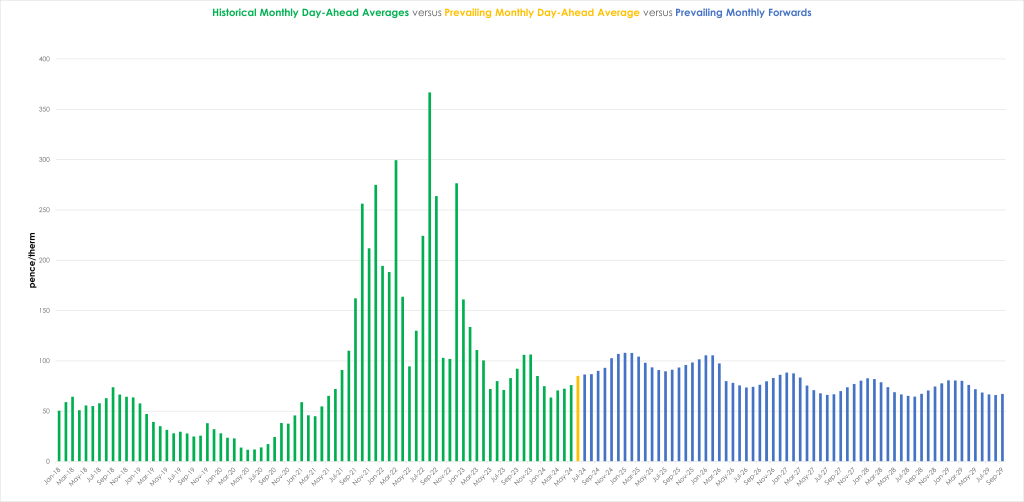

Monthly Day-Ahead averages are on target this month to achieve 85p/therm (or circa. 2.9p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, European emissions and power curve prices mirrored the sharp volatility of the gas market yesterday (driven by the unplanned Norwegian outage).

On the Carbon markets, the Dec ’24 EUA (European Allowances) retains its immutable correlation with the gas market despite key drivers pointing downward (with little development on the demand side and heavy renewables outputs).

Back in the UK, UKAs (UK Allowances) continue to drift northwards – now trading at circa. £48/tn (Dec-24 benchmark) – having broken above the highs printed on 25th Mar ’24 and having breached overhanging resistance trendlines.

Our electricity generation mix was bearish in nature today with renewables contributing 51%, thermal at 11% (gas and coal) and low carbon at 28% (nuclear and imports).

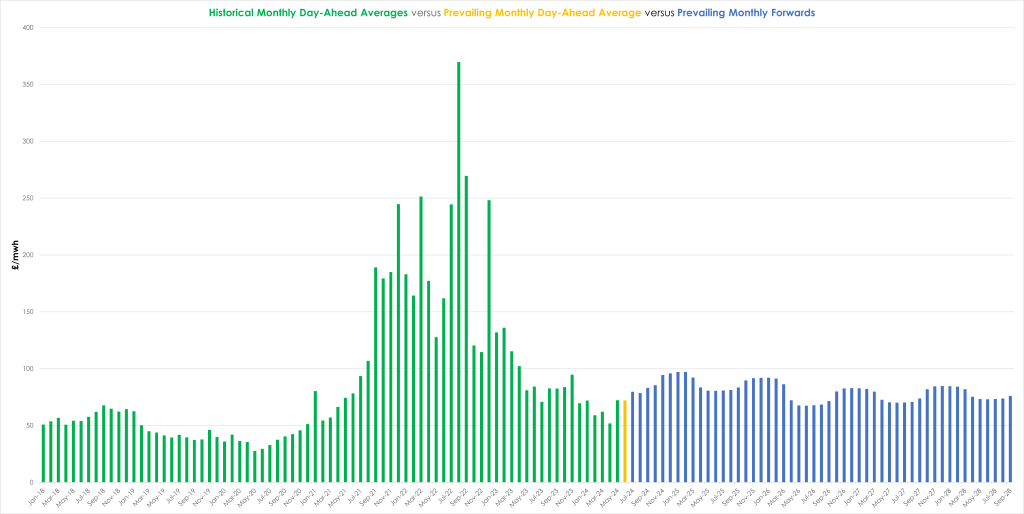

Monthly Day-Ahead averages are on target this month to achieve £72/mwh (or 7.2p/kwh excluding non-energy).