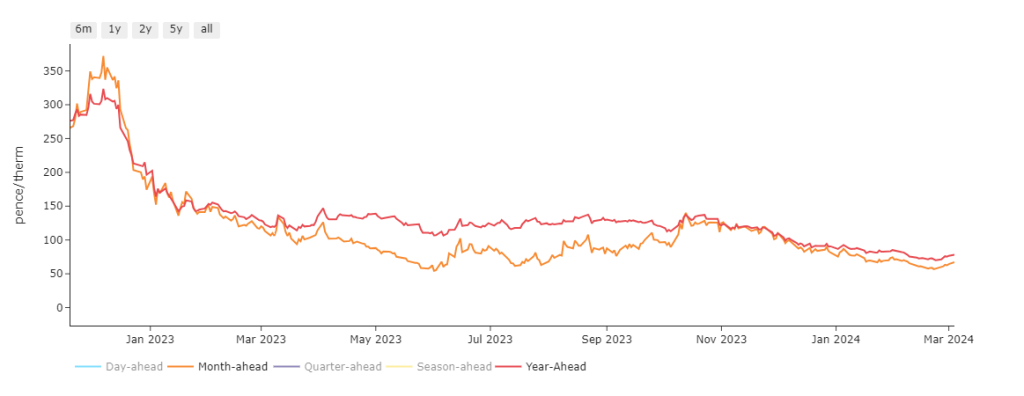

Month-Ahead prices fell below Year-Ahead at the back end of ’22, and remained there for the duration of ’23 (see chart) – near-term delivery prices are always the first to react to key drivers.

These two price lines returned to near-parity at the height of Winter-23, only to fall in unison over the last few months.

At the time of writing, the price you’ll pay for delivery next month is only at a 14% discount to the Year-Ahead price – reflective surely of the market’s belief that prices in the longer term are expected to remain steady.

Nonetheless, the last couple of days have seen near-term delivery prices lift around 8% versus a week ago.

Key drivers for this upwards correction include falling LNG flows (with arrivals waiting to be degasified having fallen circa. 13% w-o-w), cooler tmperatures expected (increasing gas-for-power burn), an unscheduled outage at Karsto in Norway (tightening supply) and (most importantly) an announcement overnight from one of America’s largest natural gas producers (EQT Corp) that, due to falling global gas values, they’ll be cutting gas production by upwards of 30% (100 billion cubic feet/day).

Not unlike OPEC, the large gas producers evidently appreciate they can impact on market values by imposing scarcity/supply tightness.

Anyway, for the time being at least, this gambit has paid off as both near- and far-term delivery contracts are finding solid support today.

26 days of Winter-23 remain, with European storage still likely to finish the winter with more than 50% left in the tank – currently at 62% versus the 5-year average of 46%.

Monthly Day-Ahead averages are on target this month to achieve 68p/therm (or 2.3p/kwh).

ELECTRICITY & CARBON ALLOWANCES

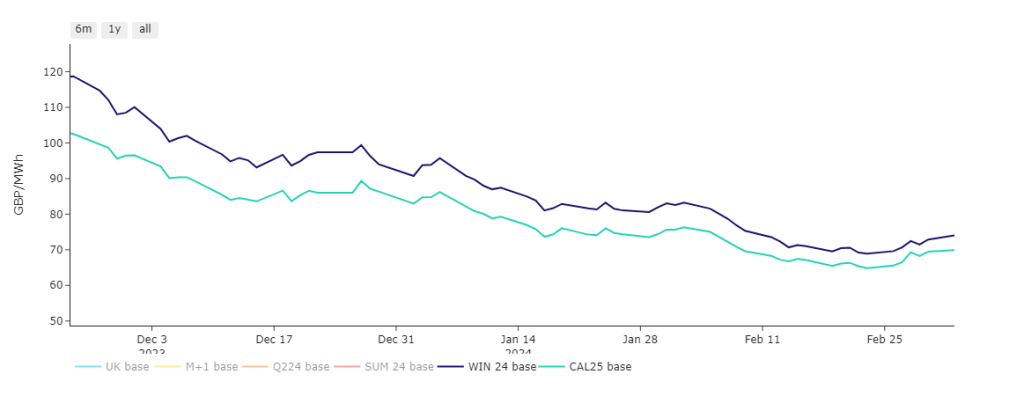

Having diverged by as much as 30% at the back end of ’22, Winter-24 and CAL-25 (calendar year) have spent the last few months drifting toward parity – reflective surely that prices in the longer term have bottomed out for the time being (see chart).

Looking to the continent, near-term delivery prices remained stable yesterday, as pressure from an anticipated rebound in wind output and early drop of fuels and emissions prices were offset by prospects of colder temperatures and weaker solar generation.

Down the curve, carbon and electricity prices experienced a particularly volatile first session of the week, starting with a steep correction in the morning as bearish sentiment took over again and markets erased the lion’s share of last week’s gains.

The subsequent steep rebound of gas prices dragged the power and carbon prices up, the EUA benchmark contract contract quickly climbing back above its 5 and 20-day moving averages.

Some analysts attributed the rapid rebound of the past couple of days to short-covering (reducing sell-exposure given oversold conditions) rather than the anticipation of a tighter supply/demand dynamic – indicating that bearish positions taken in the morning were swiftly closed once bullish momentum took hold.

The upward move remains in place today, possibly fueled as well by a downward revision of wind production forecast.

Regardless, looking at the bigger picture, fundamental drivers remain depressed, especially with the latest manufacturing PMIs showing a relapse in business sentiment.

This latest move is most likely a temporary correction of oversold conditions than it is the start of a new long-term uptrend.

Back in the UK, our electricity generation mix is bullish in nature with renewables contributing 29% and gas-for-power burn at 38%.

Monthly Day-Ahead averages are on target this month to achieve £66p/mwh (or 6.6p/kwh).