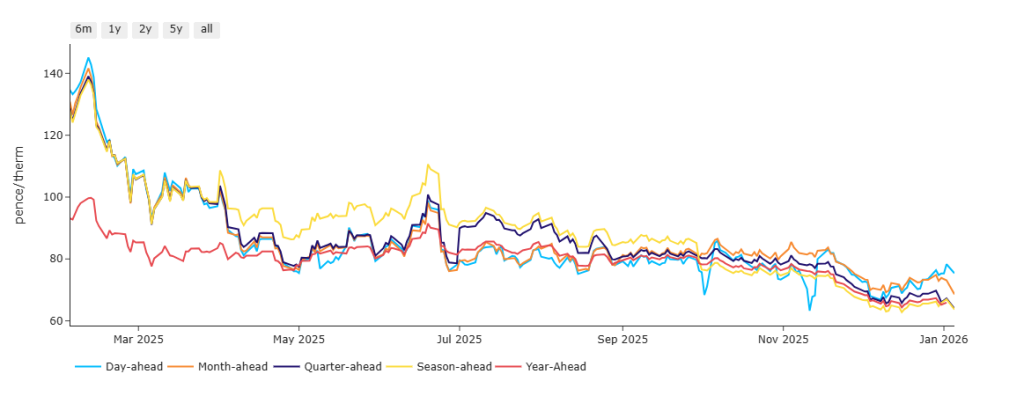

Looking at the big picture, mean-average near-term delivery prices (an aggregate of Day-Ahead/Month-Ahead/Quarter-Ahead/Season-Ahead/Year-Ahead) are at approx. 50% discount versus the highs seen last winter (posted on 10th Feb ’25) – please see chart below.

This of course reflects significantly reduced near-to-mid term risk premium, which in turn reflects more comfortable fundamentals and lower geopolitical supply risk (as yet, there have been no meaningful impacts to Trump’s capture of Venezuela’s sitting President, Nicolás Maduro).

Whilst Day-Ahead prices have inevitably risen since the onset of the UK’s current icy conditions, they’re still below or commensurate with Day-Ahead prices seen over 2025’s summer months.

Month-Ahead/Quarter-Ahead/Season-Ahead/Year-Ahead have stayed low since the onset of the cold spell, off the back of an impending global glut of LNG supply come next summer (subject to any unforeseen geopolitical impacts).

This morning, delivery contracts opened marginally higher despite the UK gas system being 10 million cubic metres ‘long’ (supply outstripping demand forecast).

Europe/the UK’s heating demand remains high due to the Arctic blast, though some forecasts promise higher temperatures and improved wind outputs by the weekend.

Generally speaking though, for the coming fortnight, wintry conditions are predicted to persist throughout northern and central Europe – not surprisingly, European storage fullness has fallen to 60% (versus a 5-year average of 73%).

On the supply side of things, Asian markets have seen a glut of Russian LNG flood their markets following the EU’s announcement that Russian LNG would be phased out by the end of this year.

So, whilst European demand is relatively ‘soft’ as a result of a milder winter, Asia’s gas take-up is also expected to remain subdued given weaker industrial outputs across China and South Korea.

All in all, we start this year where 2025 left off – solid supply amid weaker demand, and correspondingly low prices.

Monthly Day-Ahead averages for December came in at 71p/therm (or 2.4p/kwh exc. non-gas).

Monthly Day-Ahead averages for January so far are at 76p/therm (or 2.6p/kwh exc. non-gas).

ELECTRICITY & CARBON

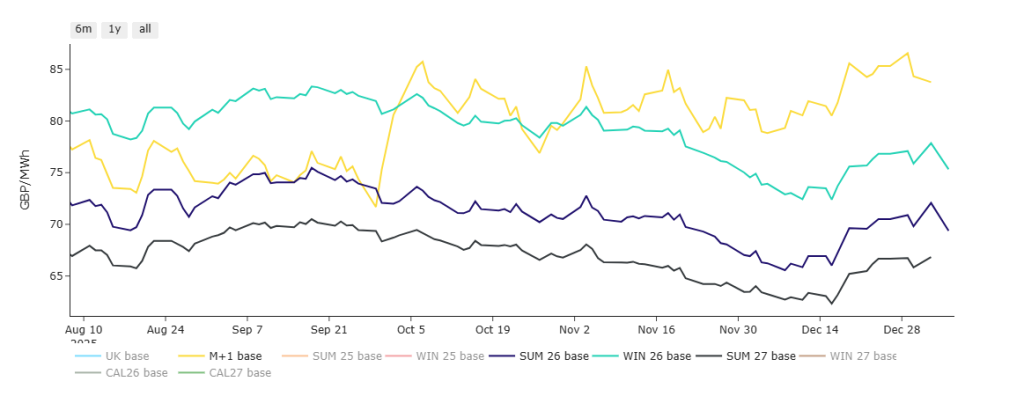

Month-Ahead delivery prices inevitably elevated off the back of the most recent cold spell – notably however, delivery prices for the front 3-Seasons (Summer-26/Winter-26/Summer-27) have been neutral-to-bearish across the same period (please see chart below).

On the Carbon side of things, UKAs went as low as £55.10 on the mid-price on 10th Dec ’25 – their lowest level since late-Oct ’25 – however, at the expiry of the Dec-25 delivery product in mid-Dec ’25, traders had supported values so as to maximise profits.

Thereafter, markets “gapped-up” to reflect the Dec-26 delivery product – though spot prices on the secondary market remain at a £2/tn discount.

At the time of writing, UKA benchmark Dec ’26 delivery is at £67.55/tn on the mid-price, with the secondary spot market at around £65.50/tn.

Today’s UK electricity generation mix is bullish in nature – specifically, renewables are contributing 21%, thermal at 55% (gas and coal) and low carbon at 8% (nuclear and imports).

Monthly Day-Ahead averages for December came in at £79/mwh (or 7.9p/kwh exc. non-energy).

Monthly Day-Ahead averages for January so far are at £94/mwh (or 9.4p/kwh exc. non-energy).