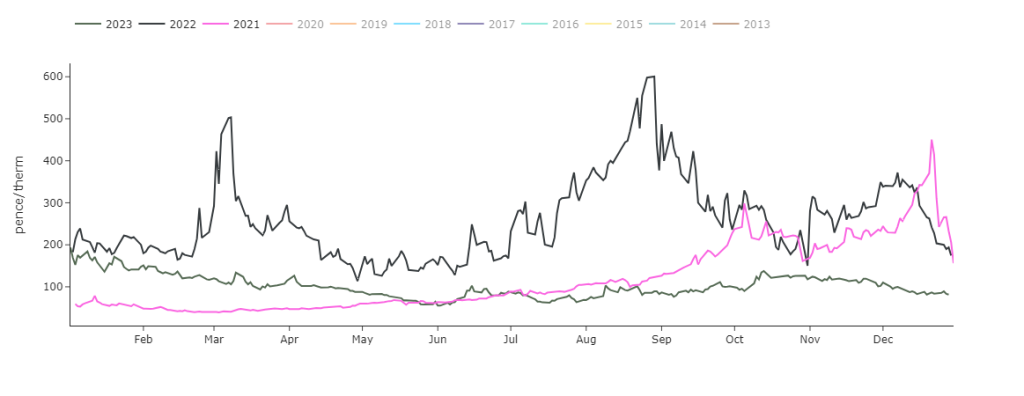

Flying in the face of historical precedent, markets continue to correct as we head deeper into Winter ’23 – a reflection surely that gas values were significantly overcooked during the energy crisis of ’21 & ’22.

See chart below detailing Month-Ahead prices for ’21/’22/’23.

Prices opened lower again this morning, and remain marginally down versus yesterday’s close at the time of writing.

Overnight, mid-term weather forecasts have flip-flopped again, making way for more downside – with lower temperatures now forecast as late as early February.

The supply-demand dynamic remains favourable with Norwegian flows at capacity, LNG arrivals on the up, historically high storage levels (notwithstanding withdrawals in Europe).

Monthly Day-Ahead averages are on target this month to achieve 82p/therm (or 2.8p/kwh).

ELECTRICITY & CARBON

Looking to the continent, a milder and windier revision of weather forecasts triggered a fall in near- and far-term delivery prices yesterday, especially on the front months.

Historically high gas and hydro storage levels, solid gas and nuclear availability against a backdrop of still structurally weak demand is keeping the pressure on prompt rates.

On the regulation side, the French government unveiled draft bill targeting a nuclear availability rate of 75% from 2030, with the goal of maintaining a nuclear fleet of at least 63GW.

Carbon followed gas prices down, with investors likely fueling the aggressive sell-off as well in an attempt to build back a strong net short position (while likely eyeing the auction resumption scheduled for 15th Jan ’24).

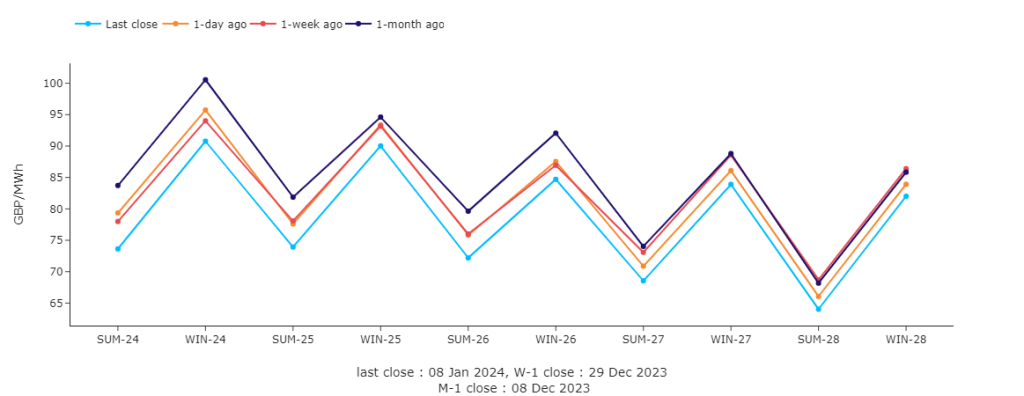

Back in the UK, Seasonal Forwards are down on the Day/Week/Month (see chart).

Monthly Day-Ahead averages are on target this month to achieve £77/mwh (or 7.7p/kwh).