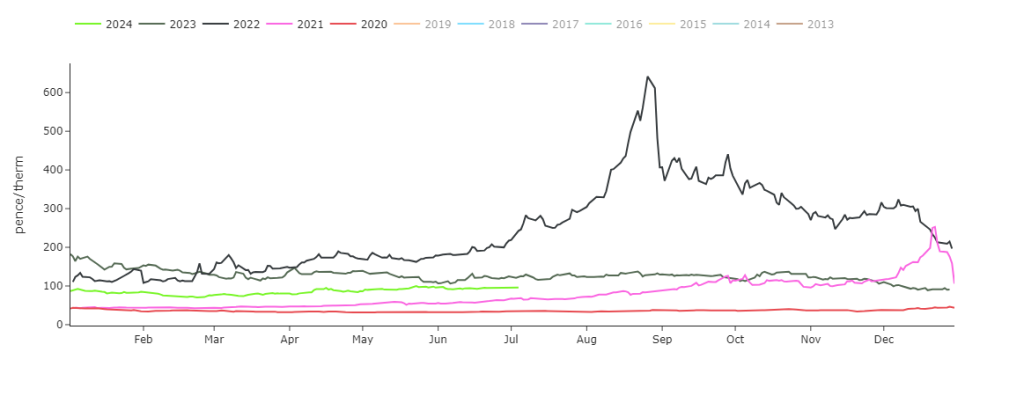

Year-Ahead prices continue to print at levels above ’20/’21, but comfortably below ’22/’23 (and notably below the psychological resistance level of 100p/therm) – see chart.

Storm Beryl came and went leaving very little damage to LNG infrastructure in her wake.

Fundamental key drivers remain soft and could result in further weakness over the coming days.

The UK supply/demand dynamic is loose (supply outstripping demand forecast).

UKCS (continental Shelf) domestic production has risen following resolution of the Tolmount maintenance.

Injections into MRS (mid-range storage) and Rough storage continue and exports to the continent remain elevated (reflecting a surfeit of gas supply).

Prices opened lower again this morning – off the back of a long UK system and deepening summer conditions.

Both Norwegian flows and LNG send out remain steady, with European storage now at 79% versus the 5-year average of 69%.

Looking at global LNG degasification w-o-w, we’ve seen a 9% fall of the number of vessels waiting to degasify for 20 days or more, coupled with a fall of 0.4 million tonnes of delivery on water – reflecting an increase in global demand most likely due to uncertainties over the impacts of Storm Beryl on US exports.

On the hedging side, we’re now on the other side of Summer-24 – with 100 days having elapsed, and 84 remaining.

Clients with open volumes for Winter-24 are increasingly scaling-in so as to avoid any loss of prevailing value.

Nonetheless, prices are soft and threatening to roll-over, with temperatures expected to be back above seasonal norms come 16th July (amid improving wind outputs as the month progresses).

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24) – though LNG delivery remains tight against a backdrop of sustained high temperatures across Asia (and the associated cooling demand).

Monthly Day-Ahead averages so far this month are on target to achieve 77p/therm (or circa. 2.6p/kwh excluding non-gas).

ELECTRICITY & CARBON

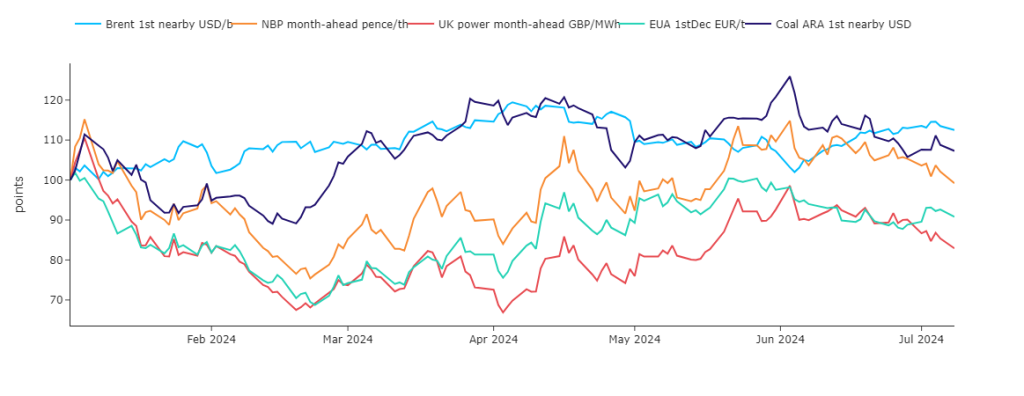

The correlation between emissions and gas prices persists – though, to some extent, the same could be said across the wider UK energy complex (see chart of relative values below).

Looking to the continent, near-term delivery prices are marginally lower off the back of strong solar generation strong over north-western Europe.

The weather outlook appears sunnier and there is potential for upward wind forecasts revisions.

Prices down the curve dropped following a decline both on the gas and carbon markets.

The impact of coal prices is also being felt, the “calendar contract” has been in a downtrend for several weeks making power from coal cheaper than gas (on some, not all, maturities).

European Carbon prices (EUAs) lost a chunk of value yesterday closing at €68.99/tonne (down circa. 2%).

Fundamentals remain bearish with high renewable outputs amid depressed industrial production forecasts.

Back in the UK, UKAs (UK Carbon Allowances) followed our prediction that prices were due to fall (as indicated by RSI divergence) – now trading at circa. £42/tonne.

Prices are now in a confirmed ascending trend channel testing the lower extremity – with £40/tn as a strong area of support to the downside – so a retest of this level is likely if EUAs can maintain bearish momentum.

Our electricity generation mix is bearish in nature today with renewables contributing 43%, thermal at 18% (gas and coal) and low carbon at 28% (nuclear and imports).

Monthly Day-Ahead averages so far this month are looking summer-esque, and are on target to achieve £61/mwh (or circa. 6.1p/kwh excluding non-energy).