Liquidity is thin and spreads between Bids & Offers are wider than usual – which reflects quiet, spiky markets.

In these conditions, it’s easy for low volume trades to move the markets more than they ordinarily would.

As such, we’ve seen an uptick to start the week, though finding reasons to support increased contract values is tricky.

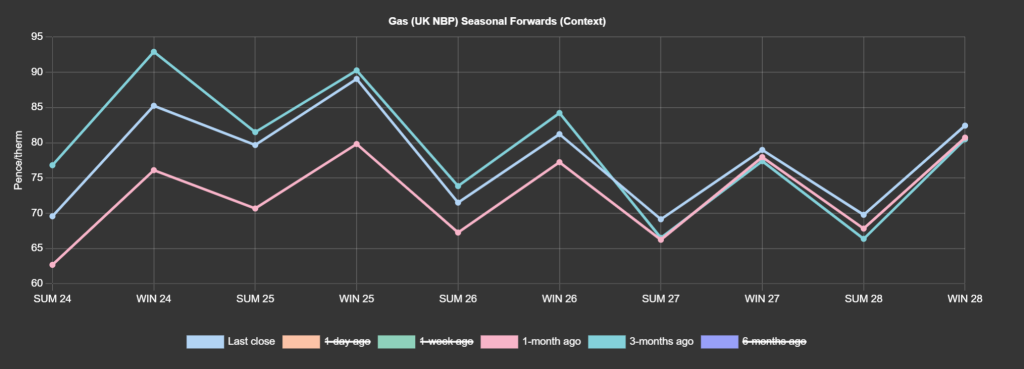

Seasonal Forwards are up on the month, but down versus 3-months (see chart).

Technically speaking, lower demand is forecast into the weekend limiting heating demand as temperatures rise.

Wind outputs are also increasing, and the warm windy conditions suggest the system balance should be nice and loose – with injections and exports required to facilitate system balance (i.e., a surplus of supply that can be stored or exported).

Supply from Norway has increased with Asgard fields due back online today, with flows expected to be at capacity over the coming days.

In short, the remainder of the week should be soft to rangebound (notwithstanding unexpected geopolitical shocks) – though prices shouldn’t fall too far considering the temperature drop below seasonal norms expected next week.

Noise aside, and in the absence of further geopolitical turmoil, it’s likely we’ll see improved value for Winter-24 delivery as the summer progresses.

Monthly Day-Ahead averages are on target this month to achieve 64p/therm (or 2.2p/kwh).

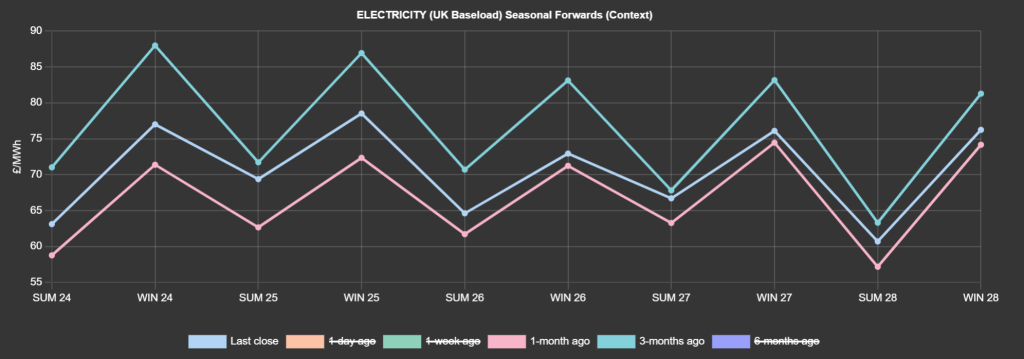

ELECTRICITY & CARBON

Looking to the continent, bearish pressure may strengthen again for the second part of the week as temperatures and solar outputs rise.

Fundamentals remain comfortable with high gas stocks, weak demand and solid renewables generation, limiting any upside scope.

On the carbon markets, prices tracked the energy complex for most of yesterday but ignored the late recovery of gas prices to instead rise before the session’s close.

The move came as a surprise to market participants – was the the sudden strength caused by speculators abandoning their bearish bet on the market or simply covering their positions ahead of the COT Commitment of Traders report)?

It’s difficult to believe that the upward move marked the beginning of a meaningful bullish rally given the still very weak industrial activity and high renewables activity/outputs.

Dec-24 contracts for UKAs are circa. £35/tn – so relatively unchanged.

Our electricity generation mix is very bearish in nature today with renewables contributing 58%, thermal at 5% (gas and coal) and low carbon at 23% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £51/mwh (or 5.1p/kwh).