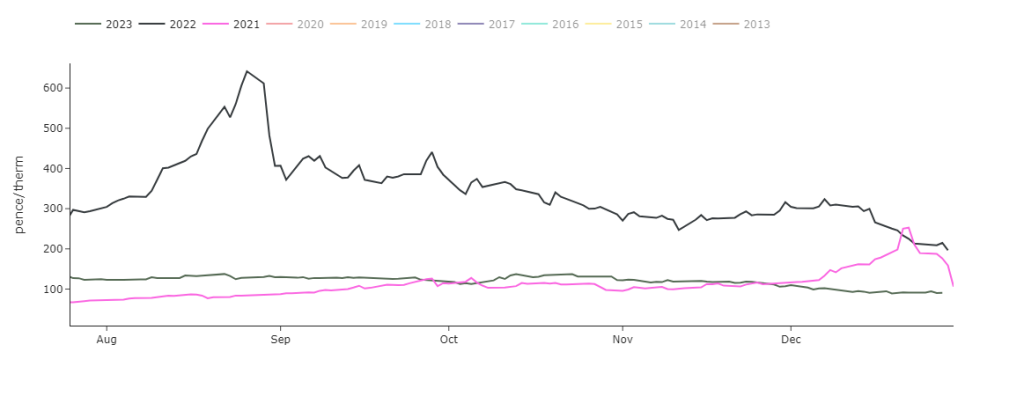

Notably, back in Sep ’21, benchmark Year-Ahead NBP gas prices rose above the psychological level of 100p/therm.

By Aug ’22, at the height of the energy crisis, Year-Ahead had risen to 641p/therm.

In Nov ’23, with very little fanfare, Year-Ahead prices fell back below 100p/therm, and remain below this level (see chart detailing Year-Ahead for ’21/’22/’23).

Markets have opened soft again this morning versus yesterday’s close.

The UK system opened long with supply outstripping demand – LNG send out is very strong (back above 100 mcm); Norwegian flows are steady; storage remains at historical highs for this time of year.

However, European storage withdrawals have been on the rise over the last week given low temperatures across the continent.

Nonetheless, inventories are at 83% fullness versus the 5-year averge of 71%.

Down the curve, prices are treading water with key drivers well balanced.

Market participants continue to eye disruptions in the Red Sea region with Houthi rebels still intent on further strikes despite the US sinking their vessels at the turn of the year.

Back in the UK, monthly Day-Ahead averages are on target this month to achieve 82p/therm (or 2.8p/kwh).

ELECTRICITY & CARBON

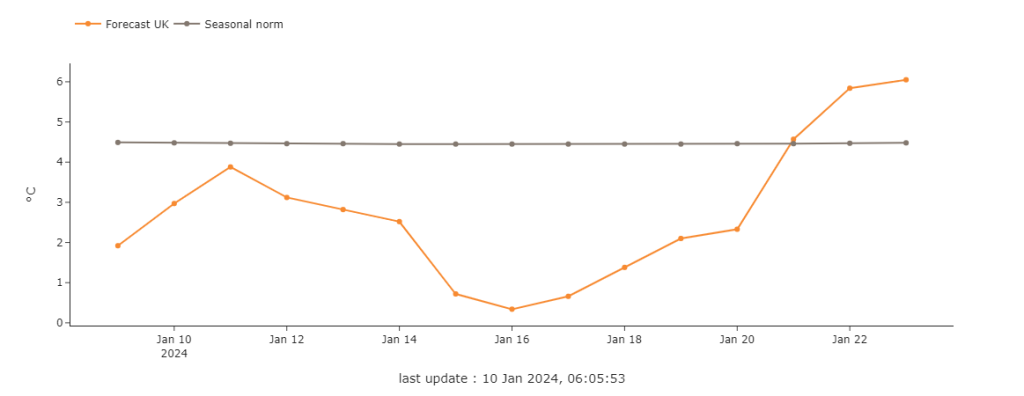

Depending on which mid-range temperature forecast is to be believed, UK temperatures look likely to rise above seasonal norms by 21st Jan (see chart).

Looking to the continent, European near-term delivery prices maintain their very gradual rise continued amidst low temperatures and forecasts of weaker wind outputs.

Considering we’re in the height of Winter ’23, bullish reaction to cold, still conditions across Europe has been muted – further reflecting a comfortable balance of structurally weak demand (i.e. temperature effect discounted) and high gas/hydro fullness.

Prices are even expected to ease in the upcoming days amid rebounding wind production, rising French nuclear availability and temperatures progressively reverting closer to seasonal norms.

Down the curve, prices are still correcting last week’s rebound off the back of more favourable temperature forecasts for the end of the month.

Back in the UK, carbon is well-balanced and trading in a tight range pending resumption of auctions this month – spot UKAs are at £36/tn at the time of writing.

Monthly Day-Ahead averages are on target this month to achieve £78/mwh (or 7.8/kwh).