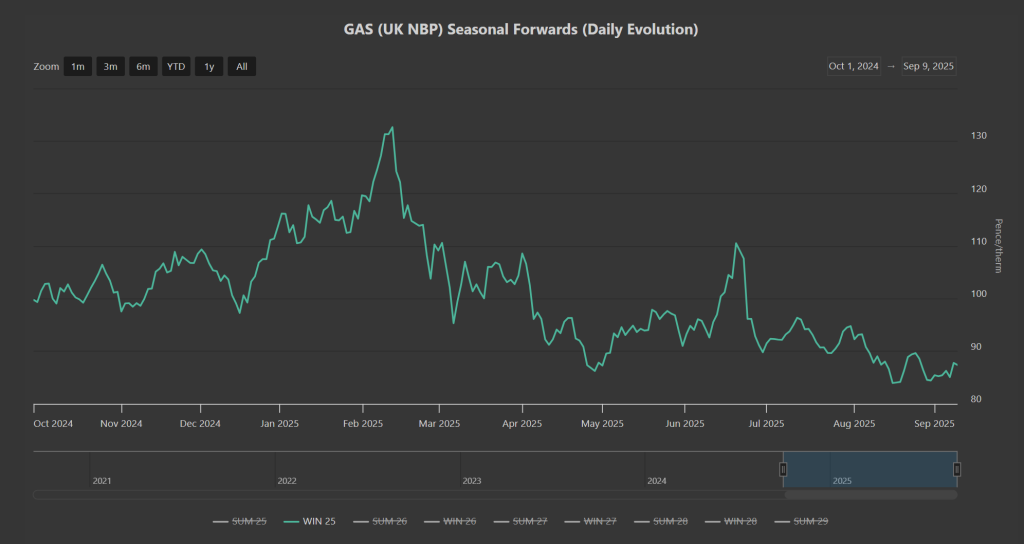

With just 21-days to go before the end of Summer-25 (and the onset of Winter-25), it’s worth noting how the Winter-25 delivery price has evolved over the past year (please see chart below).

At the start of Winter-24, Winter-25 delivery prices were 12.5% higher than yesterday’s close.

So whilst markets have felt jittery over the last 12-months, all noise aside, prices have ultimately fallen.

Notably, Summer-25’s trading range was less volatile, trading within a 21% range – whereas Winter-24 was more volatile, trading within a 27% range.

So will this summer’s low volatility continue over the coming months despite winter conditioning and ongoing geopolitical disquiet?

Well, Putin is prone to time his gambits (so as to cause the most damage) during the winter months when supply is tight, and fear and avarice are most reactive.

Indeed, today’s markets have taken on a bullish tone following reports of Russian drones entering Polish airspace overnight and subsequently being shot down.

To date, the Kremlin has deliberately avoided any direct conflict with members of NATO – a turning point?

Trump’s latest strategy with a view to controlling Putin has been to ask the EU to impose tariffs on China and India (raising the stakes should they wish to continue to trade with Russia).

With imports from Russia on the rise, China is soon likely to eclipse Germany as the world’s largest pipeline natural gas importer.

Of course, Germany has increasingly moved to LNG over the last couple of years – but this dynamic shift makes clear how the global gas market has evolved since Russia’s invasion of Ukraine in Feb ’22.

In other impactful news, Israel launched strikes into Qatar targeting Hamas leaders purported to be meeting in Doha (Qatar accounts for 20% of the world’s LNG export).

Trump is said to be unhappy with Israel, but claims to have been told about the strikes before they happened – though evidently was unable (or chose not) to stop them.

European storage fullness is now at 80% versus the 5-year average of 85% – with injections slowing (in the main) due to the climax of the Norwegian pipeline maintenance season.

Any late buyers of Winter-25 delivery are strongly encouraged to get in soon before winter conditions kick-in (and storage injections flatten come October).

Monthly Day-Ahead averages so far have been at 79p/therm (or 2.7p/kwh exc. non-gas) since the start of the month, and remain so – so, very low volatility persists.

ELECTRICITY & CARBON

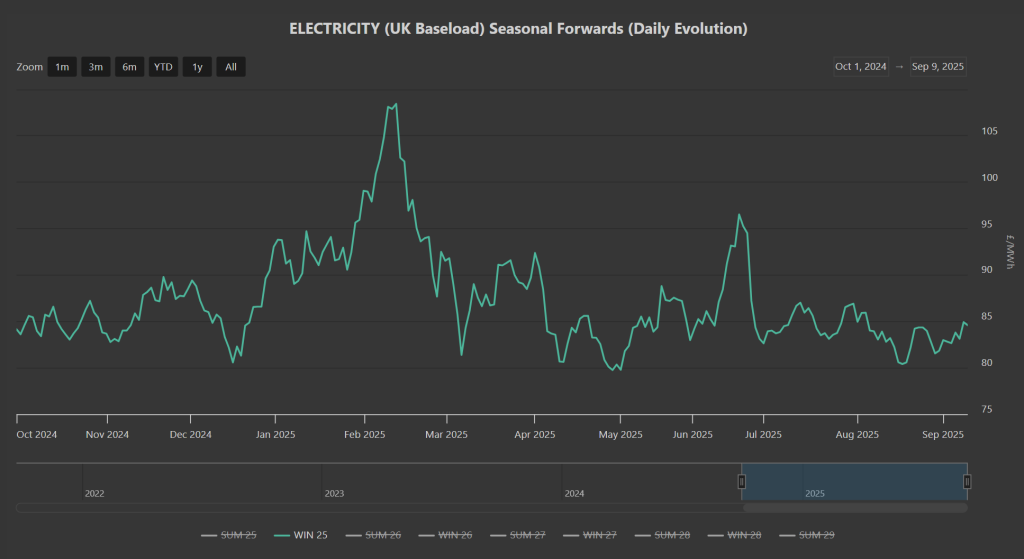

As we did with gas above, it’s worth noting how the Winter-25 delivery price has evolved over the past year (please see chart below).

At the start of Winter-24, Winter-25 delivery prices were at £84/mwh – yesterday closed at…£84/mwh!

So whilst markets have felt jittery over the last 12-months, all noise aside, prices have ended where they started.

Notably however, Summer-25’s trading range was less volatile, trading within a 17% range – whereas Winter-24 was more volatile, trading within a 26% range.

Today. prices are marginally up (in-line with firmer gas Forwards).

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices have broken to the topside off the back of the impending close to the summer season – prices having broken above further resistance levels and are at £57.26/tn on the mid-price.

Prices are now observing an upwards trend channel, with the next meaningful resistance level at £58/tn – suffice as to say, speculators have taken Carbon on a bull rally at odds with corresponding gas prices (so increasingly uncorrelated).

As such, renewed political instability and the likelihood of profit-taking would suggest we’ll see a corection downwards over the coming days.

Whilst wind outputs are improving across the UK (limiting gas-for-power burn), the continent remains a bit cold and still – though conditions are expected to become more blustery by the weekend.

Any late buyers of Winter-25 delivery are strongly encouraged to get in soon before winter conditions kick-in (and gas storage injections flatten come October).

Monthly Day-Ahead averages for the month so far are at £68/mwh (or 6.8p/kwh exc. non-energy).