The front winters (’24/’25) are back up testing 100p/therm again following last week’s short-lived drop off to 96.57p/therm.

The UK system was long at this morning’s open (supply outstripping demand forecast) with a little more Norwegian flow coming back online.

LNG stocks remain healthy despite very few arrivals to UK ports this month – sendout remains stable at 8mcm/d (million cubic metres/day).

The Wheatstone LNG platform in Australia is undergoing unscheduled maintenance meaning LNG buyers are likley to see increased competition for cargos.

Australia supplies a good chunk of its LNG output to Asia where high temperatures have increased cooling demand – so Asia will need to compete for cargos which otherwise would be headed for Europe/UK shores.

On the weather side, forecasts are mixed so expect some flip-flopping – though it’s likely we’ll not see temperatures back up above seasonal norms until the 20th.

Wind generation has dropped off a cliff but will be back up again by the weekend, then forecast to plateau at moderate levels for the remainder of the month.

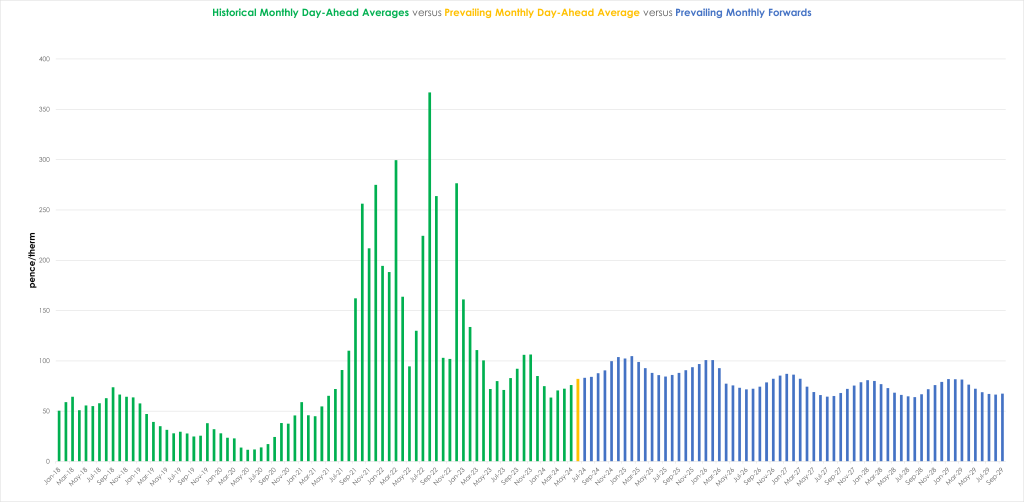

European storage is at 72% versus the 5-year average of 59%.

Global LNG production is forecast to rise 4% to coincide with the onset of Winter-24 – it’s conceivable if we have another mild winter that increased export capacity may lead to an oversupplied market next summer.

As we head deeper into summer conditioning, demand is on a downwards trend from here-on-in and will gradually loosen the UK balance – allowing storage injections.

Whilst it’s conceivable we’ve already seen the bottom of summer pricing, it’s not panic stations just yet.

The consensus amongst Industrials continues to be one of scaling-in whilst adopting a wait-and-see approach to any remaining open volumes for Winter-24/winter-25.

111 days of Summer-24 remain (with 73 days now used up) – so we’ve got the best part of two thirds of Summer-24 still to come.

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24).

Monthly Day-Ahead averages are on target this month to achieve 82p/therm (or circa. 2.8p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices cleared with mixed results yesterday – down in France (on anticipation of rising nuclear availability) but up in Germany, Belgium and the Netherlands (at the prospect of falling wind ouputs).

On the Carbon markets, EUAs (European Allowances) observed a noticeable decline in the afternoon, heading back toward the 70€/tonne level.

Market participants attribute the recent erratic moves of emissions to a combination of gas developments and technical trading (ahead of the June options expiry).

EUAs have seen bearish momentum over the past couple of weeks, and further weakness in the gas market will likely bring about a more sustained downward move.

The COT (Commitment of Traders Report) released today shows an increase in speculators’ net short position highlighting their appetite to renew a bearish bet on the market.

Back in the UK, UKAs (UK Allowances) are treading water – now trading at circa. £49/tn (Dec-24 benchmark) – having failed to break above the upper extremity of the confirmed price channel, with momentum indicators in overbought territory and rolling over (see chart).

Our electricity generation mix is bullish in nature today with renewables contributing 16%, thermal at 43% (gas and coal) and low carbon at 27% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £67/mwh (or 6.7p/kwh excluding non-energy).