As predicted (in the absence of heightened geo-political risk), markets continue to meander southwards.

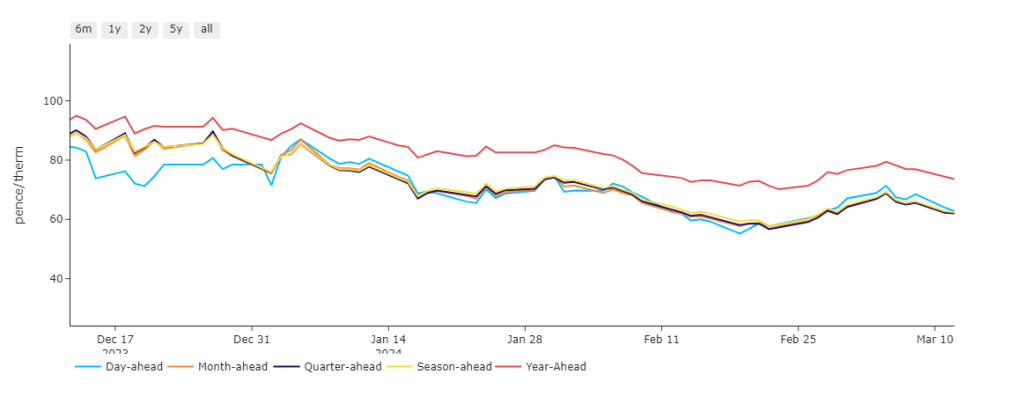

Last week’s short-covering has abated, and it’s as you were – with near-term delivery set to test the lows printed back on 22nd Feb (see chart).

Both Europe and the UK are expecting temperatures above seasonal norms for the rest of March against a backdrop of weaker demand (Industrial and domestic).

Volumes of LNG crossing European waters waiting to degasify has risen sharply by 27% w-o-w to circa. 3.5 m/t (million tonnes).

European inventories remain at historical highs – 61% fullness versus the 5-year average of 45%.

Demand forecasts remain below seasonal norms and the UK system is long at the time of writing (supply outstripping demand).

On the supply side, it’s very comfortable – the outage any Nyhamna having little impact on continually strong Norwegian flows.

Geo-political risk is background noise, with lingering shipping disquiet in the Red Sea area – though LNG is mostly headed around the Cape of Good Hope.

18 days of Winter-23 remain, and buyers are looking to summer conditioning to further soften Winter-24 offers.

Monthly Day-Ahead averages are on target this month to achieve 67p/therm (or 2.25p/kwh).

ELECTRICITY & CARBON

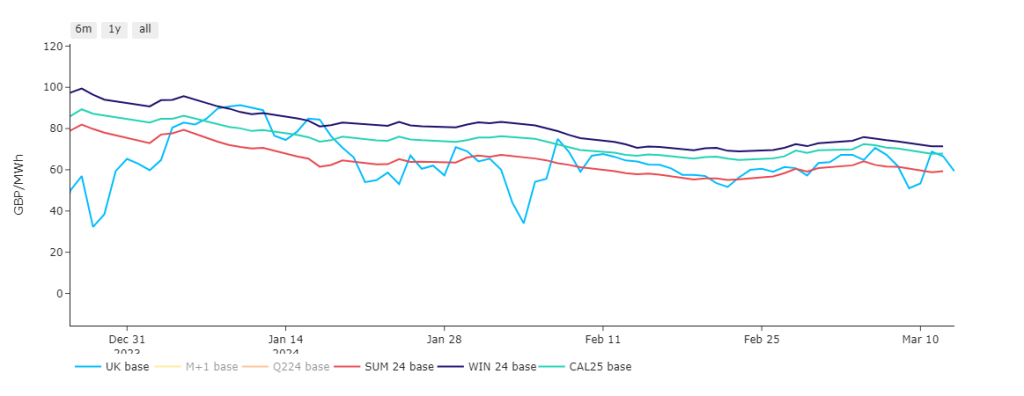

As you’d expect heading toward summer conditioning, Day-Ahead is using Winter-24 delivery prices as a resistance level (see chart).

Looking to the continent, European near-term delivery prices dropped off yesterday pressured by a resurgence in renewable outputs coupled with rapidly rising temperatures.

Expect more of the same this week off the back of windier, sunnier, and milder weather conditions.

Down the curve, markets are trading sideways having found a comfortable equilibrium – pressured by steady gas prices, buoyed slightly by firmer carbon.

On the carbon markets, market particpants are eyeing either a further short squeeze or subject to the latest COT (Commitment of Traders report), we may find that short-covering has abated – as such, speculators are likely to rebuild their net-short position and we’ll see a retest of February lows.

At the time of writing, Dec-24 contracts for UKAs are sitting at £38/tn.

Our electricity generation mix is bearish in nature this morning with renewables contributing 53%, thermal at 16% (gas and coal) and low carbon at 20% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £65/mwh (or 6.5p/kwh).