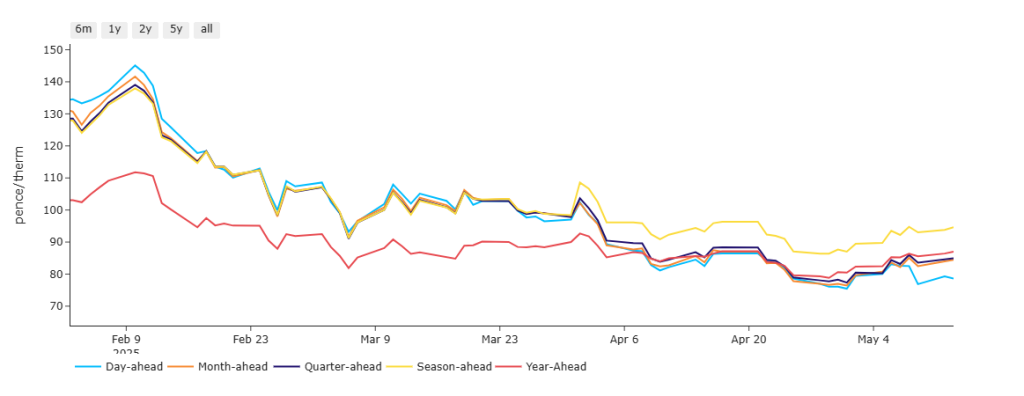

With Summer-25 now well underway, Day-Ahead prices are enjoying a discount to all other near-term periods of delivery (reflecting typical summer conditions – low demand, storage injections, benign weather) – please see chart below.

Geopolitically, it’s a tale of two key drivers right now, with market participants trying to second-guess the outcome of warming trade relations between the US and China (following a 90-day hiatus on inflated reciprocal tariffs), and a potential meeting between Putin and Zelensky being touted.

The US-China angle is bullish (giving rise to the prospect of China rejoining the battle for LNG delivery if associated tariffs are softened).

The Ukraine-Russia angle is bearish (as the re-introduction of Russian flows into Western Europe would see prices drop off a cliff).

Though, of course, the EU has reiterated its determination to stop importing any Russian gas by 2027 (notwithstanding any potential ceasefire).

On the supply side, Asian LNG demand remains weak (which allows for tempered falls in European prices i.e., our prices don’t need to stay high just to ensure cargoes don’t head to China).

The intently observed European storage levels are now up to 43% versus the 5-year average of 54% – so not too far off the pace (with solid injections off the back of warm temperatures, decent solar outputs, and low summer demand).

On the trading side, clients running flexible capability are encouraged to scale-in modest hedges over the coming days/weeks whilst the going’s good – and whilst so many geopolitical variables remain outstanding.

This month’s UK gas Day-Ahead averages have dropped off a little over the weekend, and now stand at 79p/therm (or approx. 2.7p/kwh excluding non-gas).

ELECTRICITY & CARBON

Electricity remains corrlated to gas movements (as you’d expect given the UK’s ongoing reliance on gas-for-power generation).

Notably, Winter-25 prices keep knocking on the door of £80/mwh but have yet to sustain a break to the downside.

Attempts to break below this new psychological level failed in Apr’24/Sep’24/Dec’24/Mar’25, then twice this month so far.

So it’s fair to conclude that £80/mwh (or 8p/kwh) represents the market-bottom for Winter-25 right now.

As of yesterday, UKAs (mandatory carbon credits) are dropping like a stone to re-test £48.80/tn – the bearish momentum most likely attributed to low summer demand and improved renewables outputs – please see chart below.

Today’s UK electricity generation mix is bearish in nature reflecting high temperatures and good renewables outputs – specifically, renewables are contributing 54%, thermal at 6% (gas and coal) and low carbon at 29% (nuclear and imports).

So far this month, electricity Day-Ahead averages are holding steady at £74/mwh (or approx. 7.4p/kwh excluding non-energy).

On the trading side, clients running flexible capability are encouraged to scale-in modest hedges over the coming days/weeks whilst the going’s good – and whilst so many geopolitical variables remain outstanding.