Markets started to lose ground toward the end of yesterday’s session amid rumours that the US and Iran were to reconvene peace talks in Islamabad over the coming days.

Today, the markets have continued to slide, and are at a 7-week low at the time of writing.

Whilst investment funds are still heavily net long across European benchmarks, they’re nonetheless scaling out, not in – whilst market participants in general evidently sense that Trump is running out of road.

If funds/speculators were to sense the one-way bet was over and liquidate en masse, the downside potential is, of course, very significant (considering that prevailing prices are still around 30% higher than pre-war levels).

Meanwhile, Israel and Lebanon are engaged in direct talks as diplomatic pressure mounts on the US/Israel to end the fighting.

In practical terms, the baffling blockade of the Strait of Hormuz (by both Iran AND the US) is keeping 20% of global LNG delivery offline.

On the non-geopolitical side of things, benign summery conditions are expected to persist beyond the weekend.

European storage is turning the corner, with the heating season coming to an end and injections exceeding withdrawals, with fullness now at 30% versus the 5-year average of 38%.

And so (as yet), the closure of the Strait of Hormuz is not limiting European supply – that will take a few more weeks before starting to bite.

Generally speaking, supply remains strong, with Norwegian flows higher day-on-day – this despite the maintenance season having already begun at the Troll field, then Vesterled next week.

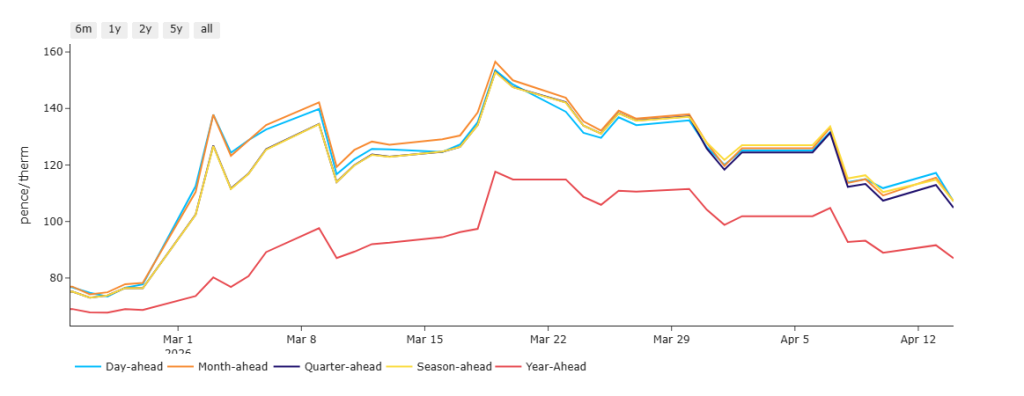

Notably, as per the chart below, Day-Ahead prices (whilst falling) have nonetheless risen back above Month/Quarter/Season-Ahead – reflecting higher near-term risk versus mid-to-long term.

Monthly Day-Ahead Averages for the month so far are lower at 119 p/therm (or 4 p/kwh exc. non-gas).

ELECTRICITY & CARBON

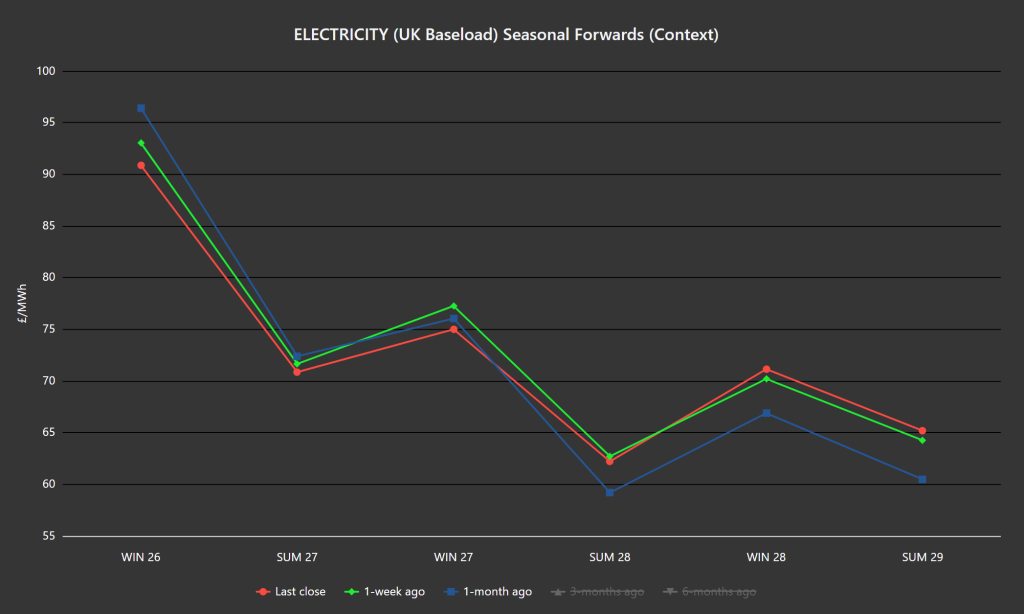

As per the chart below, the front three UK electricity Seasonal Forwards are marginally down versus 1-week/1-month ago.

UK electricity prices remain at a significant discount versus gas prices (given summer conditions/improved renewables outputs/falling gas-for-power burn).

On the Carbon side of things, Dec-26 UKA delivery remains inversely correlated to gas markets – when gas prices fall, UKAs rise (and vice versa).

At the time of writing, UKA mid-price Dec ’26 delivery is at £47.70/tn (and the spot is at mid-46s).

Monthly Day-Ahead Averages for UK electricity for the month have fallen slightly to £92/mwh (or 9.2p/kwh exc. non-energy).