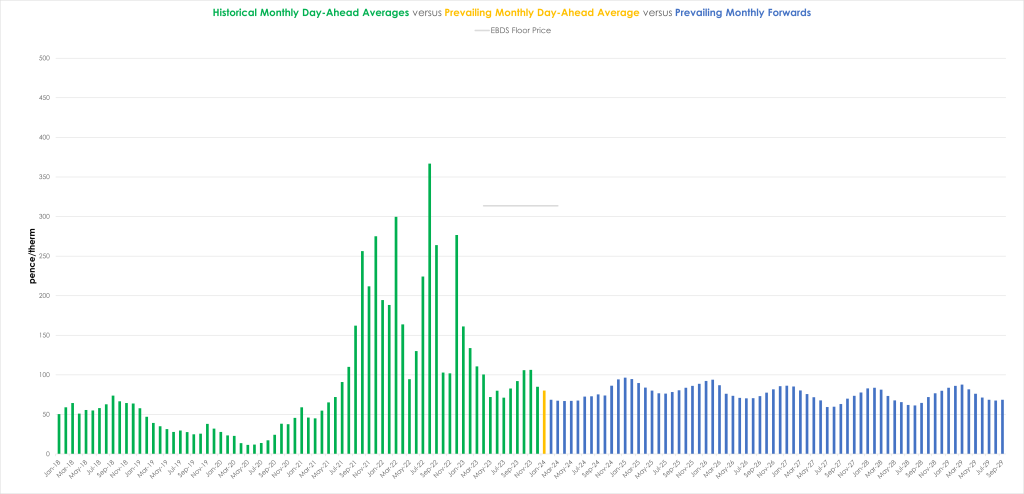

Notably, near-term delivery prices are now below those being offered for Summer-24 – despite the fact that we’re still in the thick of winter conditioning… (see chart)

In short, prices are on the slide – both near- and far-term delivery.

Prices opened down verus yesterday’s close – notwithstanding soaring demand caused by the cold spell.

UK consumption is circa. 25% above seasonal average but the UK system was still long (supply outstripping demand).

Norwegian flows remain at capacity and LNG arrivals are in rude health – offsetting any inevitable storage withdrawals.

Whilst it’s freezing right now, conditions are expected to warm up by the weekend.

Consensus is building that Europe will reach the end of Winter-23 with still over 50% of storage left in the tank.

Monthly Day-Ahead averages are on target this month to achieve 80p/therm (or 2.7p/kwh).

ELECTRICITY

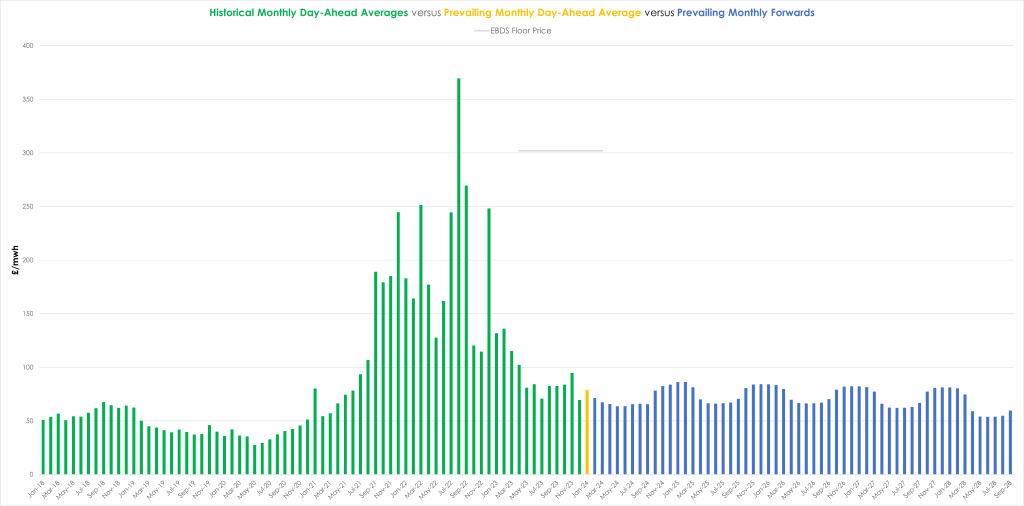

Electricity is following the gas market down with ALL periods of delivery well-under £100/mwh (see chart).

Looking to the continent, far-term delivery prices failed to sustain any meaninful rebound as participants eye the looming bearish fundamentals of strong renewables output and temperatures rising above seasonal norms.

Meanwhile, structural demand remains very low and French nuclear availability is consistently strong (& outages nowhere to be seen).

Back in the UK, our generation mix is actually bullish at 57% fossil fuels (inc. 3% coal).

Monthly Day-Ahead averages are on target this month to achieve £79/mwh (or 7.9p/kwh).