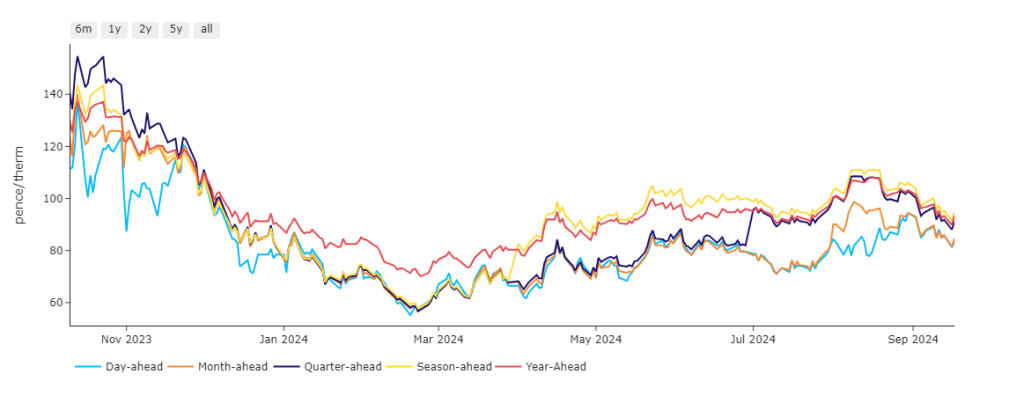

Day-Ahead has returned to parity with Month-Ahead, both of which are at approx. 9% discount versus Quarter/Season/Year-Ahead (see chart below).

The Indian Summer for bears persists with market participants (poised for the onset of Winter-24 in 13-days’ time) seemingly happy to take profits after a summer of increases and to watch front-seasons drift lower.

Down the curve, prices are lingering at a seven-week low, mainly driven by high storage levels (93% versus the 5-year average of 86%) and a sluggish overall gas demand across Europe ahead of the heating season.

Markets opened very marginally down again this morning off the back of scheduled Norwegian maintenance increasingly coming to an end with flows through Langeled to the UK coming back online – still well below capacity but running nonetheless.

The lion’s share of remaining European offline capacity is expected to resume next week barring any last-minute extensions to maintenance.

Notwithstanding significantly reduced flows into the UK (due to maintenance), our system remains long this morning (supply outstripping demand forecast).

Geopolitical risk premiums have diminished for now, notwithstanding Hezbollah suffering an unexpected attack on their operatives through mass explosions of electronic pagers yesterday (most likely at the hands of Mossad, Israel’s secret service).

Clients with significantly open volumes for Winter-24 are in the minority – with most having opted to heavily hedge Positions with winter conditions now on the horizon.

Monthly Day-Ahead averages so far this month are on target to achieve 86.8p/therm (or approx. 2.962p/kwh excluding non-gas).

ELECTRICITY & CARBON

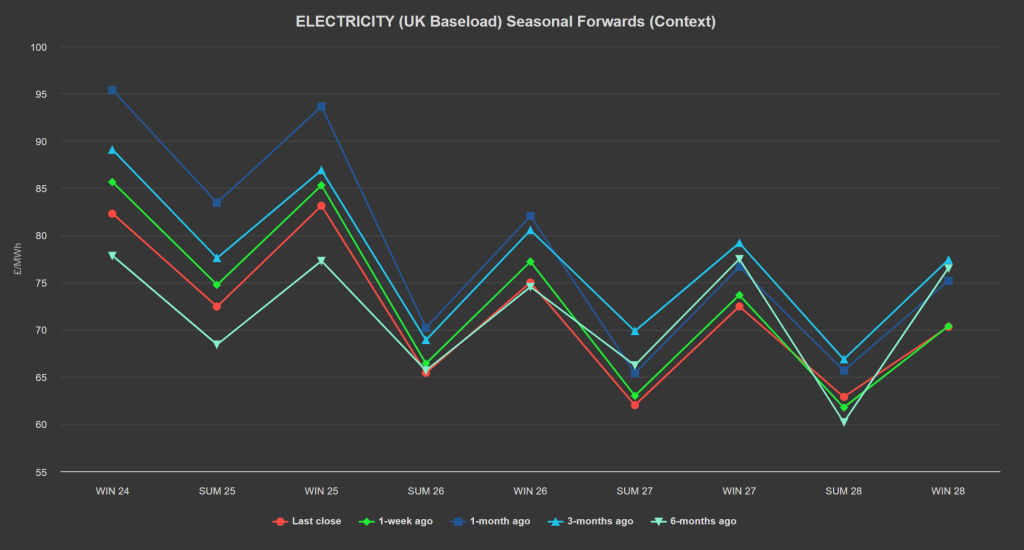

UK Seasonal Forwards closed yesterday down on the week/month/3-months ago (see chart below).

Looking to the continent for signals, temperature forecasts have been revised warmer for the end of next week, with a mild easterly flow transitioning to a westerly flow, and potential brief cooling early next week.

Wind generation has been revised upward, with strong easterly flow bringing decent generation short-term, followed by a weekend decrease and a significant ramp-up next week.

Solar generation benefits from a sunny anticyclonic pattern this week, but may face cloudier conditions next week.

Hydro conditions show dry patterns in western regions short-term, with wetter weather expected in Central-Western Europe this weekend and early next week, and a majority of forecasts indicating seasonal to above-normal precipitation after mid-next week.

On the carbon markets, Dec ’24 EUA benchmark is still showing some weakness relative to gas prices.

It closed yesterday at €64.34/tonne – whilst UKAs have dropped off a cliff this last few days, almost as a lagged response to EUA’s falls this last couple of weeks.

UKAs look set to retest £39/tonne which marks the bottom of a daily descending trend channel.

Our electricity generation mix is bullish in nature today with renewables contributing 26%, thermal at 31% (gas and coal) and low carbon at 24% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £76.829/mwh (or approx. 7.68p/kwh excluding non-energy).