Indications surfaced late yesterday afternoon that both the US and Iran were open to a resolution.

Rumours then circulated that Trump was on the verge of relenting, stating that U.S. could “end the military campaign within two to three weeks and that Iran does not have to make a deal to end the conflict” – thereafter, in the last hour of the session, prices began to slide.

This morning, that slide is just about holding – though, of course, fears persist that it just might be a another false dawn/market manipulation on the part of the Trump Administration.

And yet, it does feel different today, the Iranian President, Masoud Pezeshkian, has stated that Tehran has the “necessary will” to end the war provided its enemies guarantee it will not flare up again.

Furthermore, Trump will make an announcement this evening from the Whitehouse at 9pm EST (so in the early hours of the morning GMT).

He’s expected to confirm that the US will pull out of Iran in the coming weeks, as well as reiterate his intentions to pull out of NATO (true to form, he’s unlikely to consult with Congress on the matter).

Starmer has put himself forward to host multinational talks this week over the Strait of Hormuz, and how the world might clear up the mess left behind if/when the US calls it a day.

Markets are reacting favourably across the board – stockmarkets are up, oil fell back below $100 (but has now returned to $107).

In practical terms, whilst prices are widely lower, LNG prices will need to remain supported due to the significant damage at Qatar’s LNG facility (with 4% of global LNG production taken offline for several years).

The name of the game over the coming weeks will be a push toward winter restocking across Europe, which of course will be made significantly easier if/when the Strait of Hormuz re-opens.

However, if Trump leaves with the Iran regime still in place, the rest of the world will need to wrestle with potential tolls to cross the waterway (a new revenue stream that Trump’s offensive has disastrously uncovered).

Also, ship insurance to get across the Strait will need to remain inflated and so the cost of LNG will need to reflect the increased cost of transit.

Of course, the US (as the world’s largest net exporter of LNG) is unlikely to care – Trump will no doubt be eyeing the inevitable windfall that’s to come!

As was the case with Putin, Europe and the UK have once again fallen foul of naively relying on an autocrat to play fair.

Poor King Charles is being asked to go make nice with Trump at the end of April in a state visit to the US – fears abound that Trump will use the opportunity to further talk down Britain’s relevance on the world stage.

Looking at non-geopolitical fundamentals, Europe’s storage fullness is at 28% versus the 5-year average of 37% – so not great.

But Summer-26 is here, the sun is shining, and wind outputs are favourable.

For buyers, the next few days will pose a tricky conundrum – the majority of heavy-users have opted to hedge heavy at the front-end to see how things develop.

However, Investment Funds forever on the search of a one-way bet will no doubt be closing long positions to lock-in profits, but will jump back in at the first sign of trouble – which will take the market higher.

So, for the time being, whilst prices are holding their ground, we still have to remember that it’s a bulls’ market and value for near-term delivery should be secured in the dips as the summer progresses.

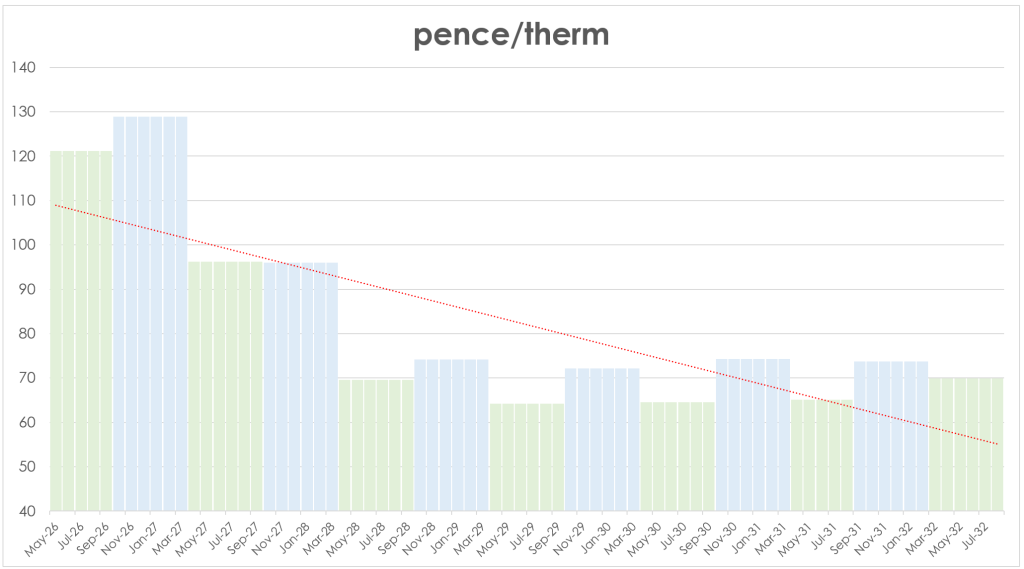

The chart below shows Seasonal Forwards (inc. Balance of Summer-26) – future prices remain heavily discounted versus near-term delivery and so favours long-term hedges.

Lest we forget, Trump is in the White House until at least 2029 (notwithstanding impeachment) – so we’ve potentially got a few years of insecure supply dynamics with which to contend.

Monthly-Day Ahead Averages for March finished at 131p/therm (or 4.45p/kwh exc. non-gas).

ELECTRICITY & CARBON

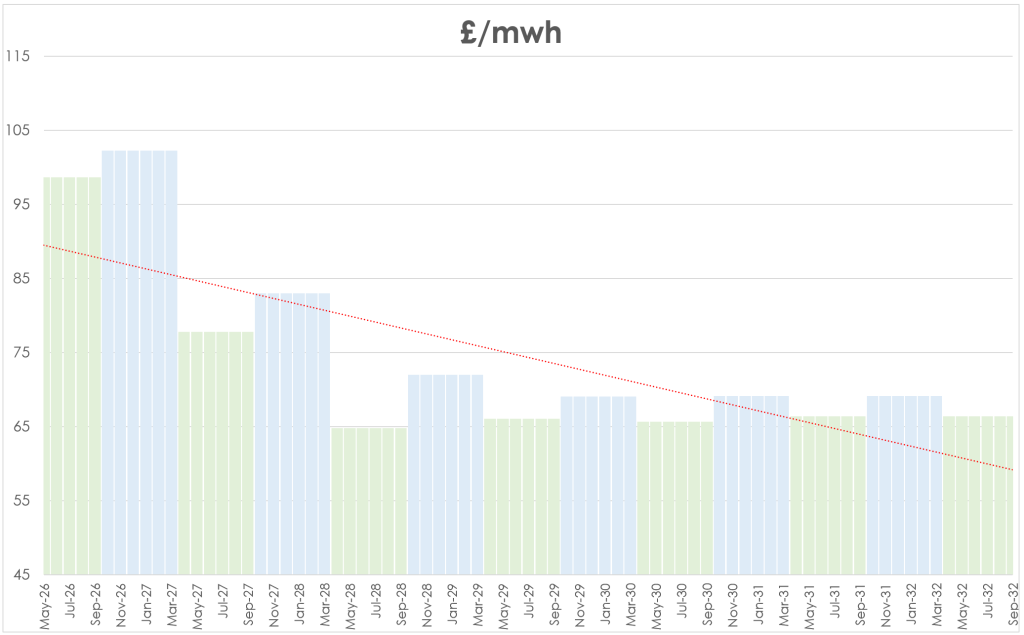

Again, the chart below still thankfully reflects an optimistic future electricity market despite the impacts of the last few weeks.

On the Carbon side of things, Dec-26 UKA delivery remains uncoupled from gas volatility with prices touching levels that are 33% below those printed in mid-Jan amid fears that Trump’s war on Iran is slowing global economies (and, in so doing, Industrial outputs).

At the time of writing, UKA mid-price Dec ’26 delivery is at £41/tn (and the spot is at mid-39s).

Over the last couple of weeks, when gas falls, UKAs firm up – and vice versa.

So, not surprisingly, UKAs are finding support this morning.

Monthly Day-Ahead Averages for March for UK electricity finished at £105/mwh (or 10.5 p/kwh exc. non-energy).