With many businesses on partial shutdown for the holidays, and trading floors/liquidity enjoying a summer lull, markets have meandered lower still amid benign fundamentals, an increasing likelihood that European storage fullness will hit mandated requirements in time for the heating season (Winter-25), and an underlying optimism amongst market participants that Russian flows may still find their way back into Europe.

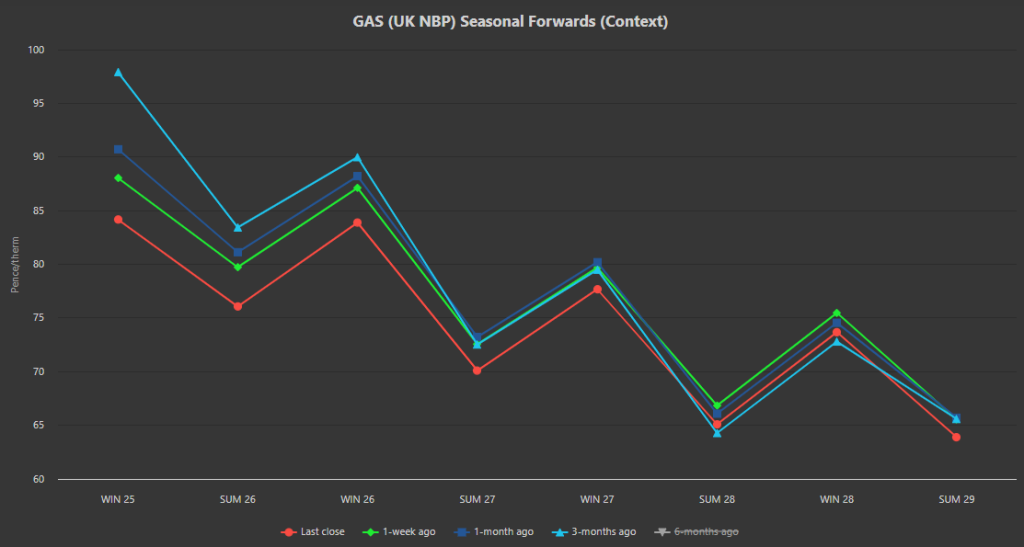

The front 5 Seasons are down on the week/month/3-months – please see chart below.

Norwegian outages are likely to pick up next month, so this late summer dip has another couple of weeks to develop before focus will shift to Winter-25 storage, and the potential impacts of mid-to-long range weather forecasts.

Any late buyers of Winter-25 delivery are still advised to get in before the 2nd week of September at the very latest.

Further to the Russia-US summit (at which Trump seemed to concede advantage to Putin), the subsequent meeting between the US, Ukraine and various other European leaders has ‘security guarantees’ at the core of negotiations.

Ukraine is looking to ensure its security from Russia going forward (presumably in exchange for accepting Russia’s permanent annexation of certain territories), whilst Europe strains to remain relevant.

It remains to be seen if Ukraine will get some land back as part of a wider deal.

Monthly Day-Ahead averages for the month so far are at 78p/therm or 2.65p/kwh (all but unchanged from the start of the month, reflecting very low-short term risk).

ELECTRICITY & CARBON

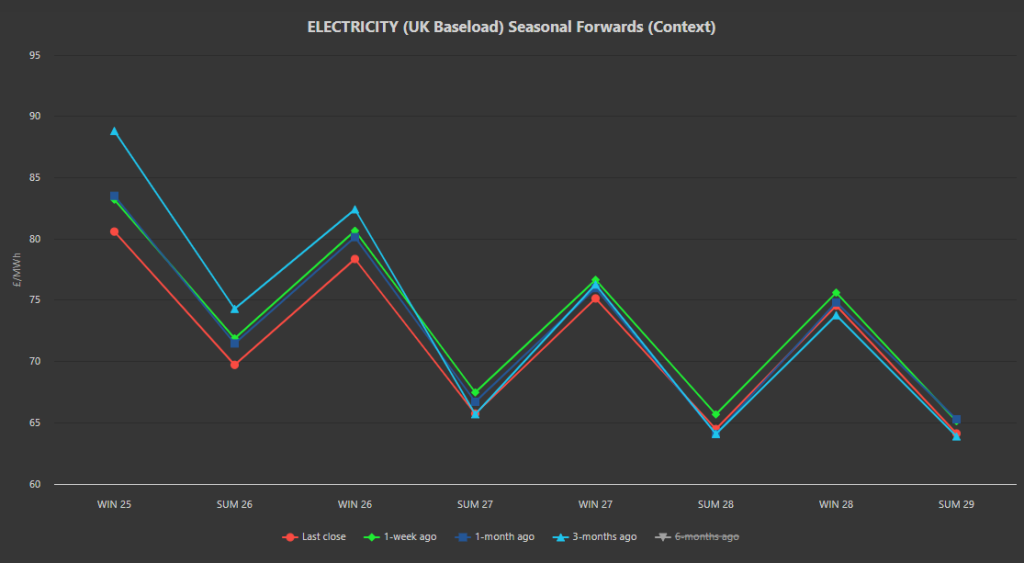

The front 5 Seasons are down on the week/month/3-months – please see chart below.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are at £50.32/tn on the mid-price, and are threatening to fall further having broken below well-established support levels.

Today’s UK electricity generation mix is neutral in nature – specifically, renewables are contributing 35%, thermal at 29% (gas and coal) and low carbon at 18% (nuclear and imports).

Monthly Day-Ahead averages for the month so far are at £70/mwh (or 7p/kwh exc non-energy).