Markets are balanced this morning, with prices treading water in a tight range above 100p/therm.

Trump’s latest gambit to extend the ceasefire, pending an agreement being reached, means a resolution is starting to look a bit open-ended.

Meanwhile, US destroyers continue to arrive in the Middle East loaded with elite combat forces – would Trump risk ordering a ground offensive?

Traders are left wondering if Trump has an end-game in mind that is informing his behaviour, or if his actions are all off the cuff.

Is it in Trump’s interests to keep the Strait of Hormuz shut?

Well, as we’ve mentioned in previous bulletins, the US was the world’s largest exporter of LNG in 2025.

With the Strait closed, China is bearing the brunt of LNG demand destruction with imports significantly down y-o-y.

And so, China’s access to LNG is greatly reduced by Trump’s actions – as is their access to oil (45% of China’s imports transit via the Strait)

Notably, China’s independent “teapot” oil refineries are heavily reliant on discounted Iranian oil, which is also being held-up by Trump’s blockade.

For the time being then, China is relying almost entirely on strategic reserves to cushion economic shock, though a prolonged closure of the Strait will inevitably threaten mid-to-long term economic stability.

Does this play into Trump’s hands in advance of the US/China summit next month?

Interestingly, just a few hours ago, Trump has suggested that the US has apprehended a Chinese ship (sic): “We caught a ship yesterday that had some things on it, which wasn’t very nice — a gift from China, perhaps, I don’t know, I thought I had an understanding with President Xi, but that’s alright.”

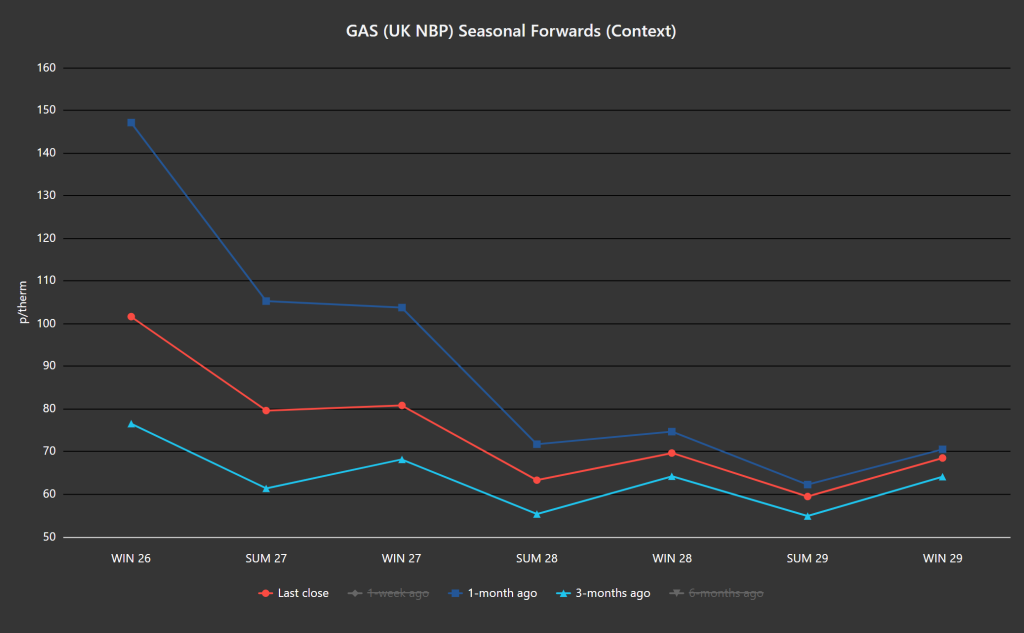

All noise aside, whilst markets remain elevated versus pre-war levels, they remain down on the month but up versus 3-months ago (please see chart below).

European storage has turned a corner with the heating season now in the rear-view mirror – so net injections have replaced net withdrawals.

Storage fullness is at 31% versus the 5-year average of 39% – so not too far off the pace.

On the trading side, FLEX clients are all but closed-out for May in the hopes that, come June, the Strait will re-open and essential LNG transit will have been restored – thereafter, low summer Day-Ahead prices will resume.

For now, however, the jury is out pending whether the prevailing impasse can be overcome.

Monthly Day-Ahead Averages for the month are headed in the right direction – now at 113 p/therm (or 3.9 p/kwh exc. non-gas).

ELECTRICITY & CARBON

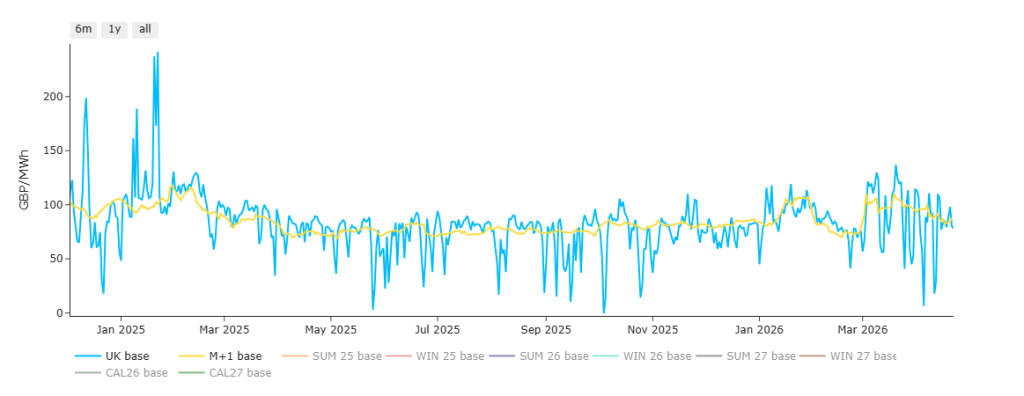

UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb.

Nonetheless, as illustrated in the chart below, the percentage variance of Day-Ahead prices (blue line) since the beginning of 2025 to date has been 158% (a low of £28/mwh, a high of £241/mwh) – where as the percentage variance of Month-Ahead (yellow line) for the same period has been only 47% (a low of £71/mwh, a high of £115/mwh) – of course, percentage change numbers would be much higher.

Suffice as to say, given summer conditions (improved renewables/lower gas for power burn), UK electricity prices remain comfortably below the psychological level of £100/mwh.

On the trading side, FLEX clients are all but closed-out for May in the hopes that, come June, the Strait will re-open and essential LNG transit will have been restored – thereafter, low summer Day-Ahead prices will resume.

For now, however, the jury is out pending whether the prevailing impasse can be overcome.

On the Carbon side of things, Dec-26 UKA delivery began the conflict heavily correlated to gas markets – so when gas prices fell, UKAs rose (and vice versa).

However, given this week’s volatility in UKAs, having fallen £3/tn since yesterday, we increasingly see a correlation with equities/stock-indices.

At the time of writing, UKA mid-price Dec ’26 delivery is at £47.78/tn (and the spot is at mid-46s).

Monthly Day-Ahead Averages for UK electricity for the month have fallen again to £88/mwh (or 8.8 p/kwh exc. non-energy).