Volatility persists amid fears over replenishing European storage levels in time for the onset of Winter-25 (coupled with an untimely outage at the Freeport LNG terminal in Texas caused by a winter storm).

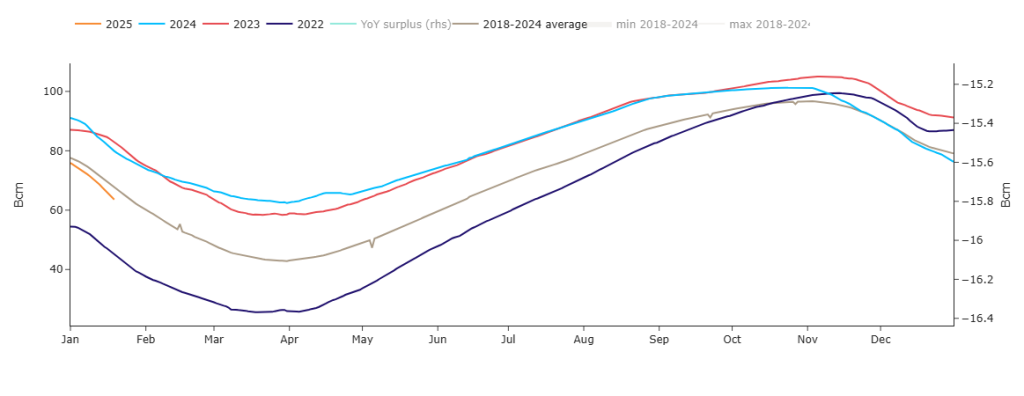

Whilst current levels are tracking just below the 7-year average (please see chart below), it’s notable that inventories are well below ’23 & ’24 (but still well above ’22).

So, what’s the worry? Surely these worries are with us every winter?

Well, IF the winter ends and storage is too low, the subsequent demand to replenish will put pressure on supply dynamics (IF this coincides with increased Asian demand come the New Year).

Withdrawals have been high this past week, which has given participants the jitters IF it should continue.

Bullish momentum has also been stoked following a release by Germany’s natural gas boss (THE) regarding a plan to enable stockpiling for Winter-25 (which bullish participants regard as a concession that a problem already exists, whereas bearish participants accept that pre-emptive measures to ensure organised replenishing of stocks is just prudent).

Unfortunately, the market remembers that a similar intervention by THE was primarily responsible for the surge in prices over Summer-22.

In summary, the document issued by THE suggests that operators be subsidised to fill storages – given the prevailing premium of Summer-25 versus Winter-25 prices.

Looking forward, temperatures are expected to gradually increase back above seasonal norms in most European countries, which should reduce heating demand.

Also, steady Norwegian flows are helping to keep a lid on the upside.

The front six Seasons are up versus /1-week/1-month/3-months/6-months ago – so it’s safe to say Forward prices are high and wintry.

As has been the case since 7th Jan, Day-Ahead prices remain more expensive than Month/Quarter-Ahead, reflecting very short term risk premia (and an underlying sentiment that improved value is available for contracts further out).

Monthly Day-Ahead averages for this month are at their peak so far off the back of low temperatures/poor renewables generation – 121.161p/therm (or approx. 4.134p/kwh excluding non-gas).

ELECTRICITY & CARBON

As is always the case (to a greater or lesser degree), UK electricity prices are mirroring gas moves – though swings are less impactful (given that end-users pay more for “non-electricity” these days, than for the commodity itself).

Today’s UK’s electricity generation mix is again bullish (and very price supportive of Day-Ahead) with renewables contributing only 7%, whilst thermal is at 61% (gas and coal) and low carbon at 17% (nuclear and imports).

Monthly Day-Ahead averages for this month so far reflect wind generation still well below seasonal norms (and increased gas-for-power burn) – £123.851/mwh (or 12.39p/kwh excluding non-energy).

On the Carbon markets, UKAs remain at a yawning discount versus EUAs – reflecting less scarcity of credits (with free allowances not scheduled to fall in the UK until 2027).

As the time of writing, the mid-price is again observing a downward trend channel and its associated support/resistance levels (please see chart below) – mid-price is currently at £32.62/tn.

However, positive divergence on the hourly RSI looks bullish – so prices look likely to retest mid-33s.