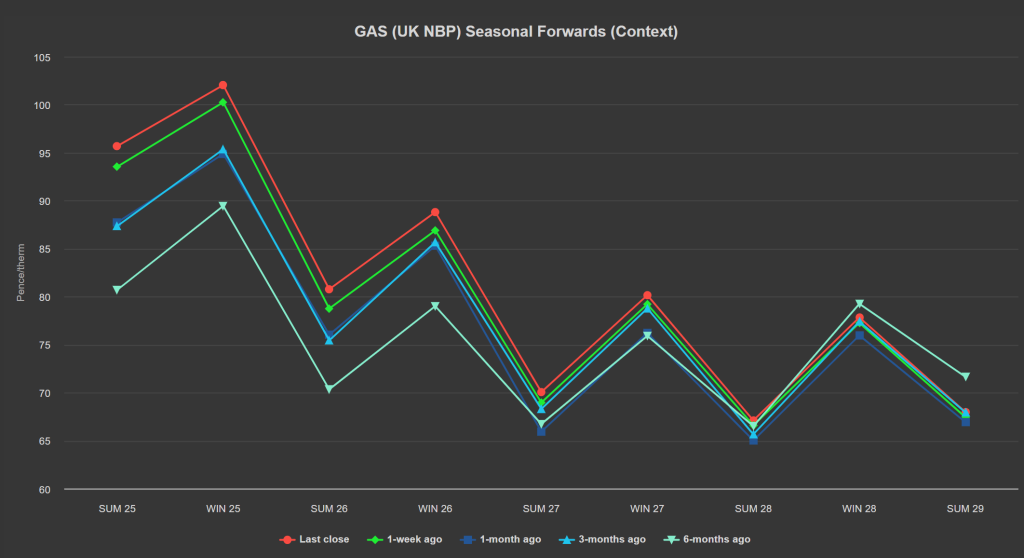

Prices are starting to feel wintry – Seasonal Forwards are up versus 1-week/1-month/3-months ago/6-months ago (see chart below).

Day-Ahead prices have now risen above Year-Ahead prices reflecting the wintry tone of near-term delivery.

Norwegian outages remain a primary supportive element, as does a shortage of LNG arrivals to UK shores against a backdrop of global conflict.

Yesterday’s price spike could be attributed to smoke being detected at the Sleipner field in Norway – leading to 7 million cubic metres of flow going offline.

On the geopolitical side, leaked rumours of Israel’s imminent attack on Iran has given market participants the jitters.

In more bullish news, the UK system opened long today (supply outstripping demand forecast) off the back of a significant reduction in storage injections.

It’s fair to argue that European prices need to rise to attract more LNG cargos to our waters (and away from Asia).

On the weather side, expect warm conditions for the time of year coupled with poor wind outputs (increasing gas-for-power generation).

Solid European storage at 95% (versus the 5-year average of 97%) is keeping a lid on bullish momentum.

Notably, Russia’s pipeline exports to China are up 40% y-o-y – meaning Russia is now exporting more gas to Asia than it does Europe.

It’s likely these exports will increase still further with the completion of the Far Eastern pipeline in 2027.

However, Chinese demand remains in question, with recent economic indicators reinforcing fears of deflation and the need for meaningful stimulus measures – though the Communist Party remain reluctant to devalue the yuan and trigger capital flight (which seems inevitable).

Monthly Day-Ahead averages so far this month are on target to achieve 96.871p/therm (or approx. 3.305p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, French nuclear generation is now forecast to the high range of the previous years.

EUAs began yesterday on a bearish note, rapidly making a €61.27/tn low early in the day.

However, it quickly recovered making a €62.56/tn high by noon off the back of rising gas prices.

Nonetheless, the Dec ’24 benchmark contract is making lower highs, day on day – reflecting a modest but defined downtrend underway.

Conversely, UKAs persist on an independent bull run – now at the upper extremity of descending trend channel that is the wider downtrend which began back in Jul-24.

For now, compliance buyers appear to be sitting on the sidelines waiting for the speculators to complete their revised positioning.

Fundamentally, the fall in UKAs over the summer was attributed to market participants’ reaction to UK policy review (or the Free Allocation Review).

The outcome being that the expected scarcity of UKAs come 2026 has now been pushed back to 2027 – resulting in speculators reducing long (buy) exposure.

However, the recent bull run is evidence of investors scaling back-in at lower levels given the great value on offer this last couple of weeks.

Our electricity generation mix is neutral in nature today with renewables contributing 36%, thermal at 33% (gas and coal) and low carbon at 13% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £80.030/mwh (or approx. 8.030p/kwh excluding non-energy).