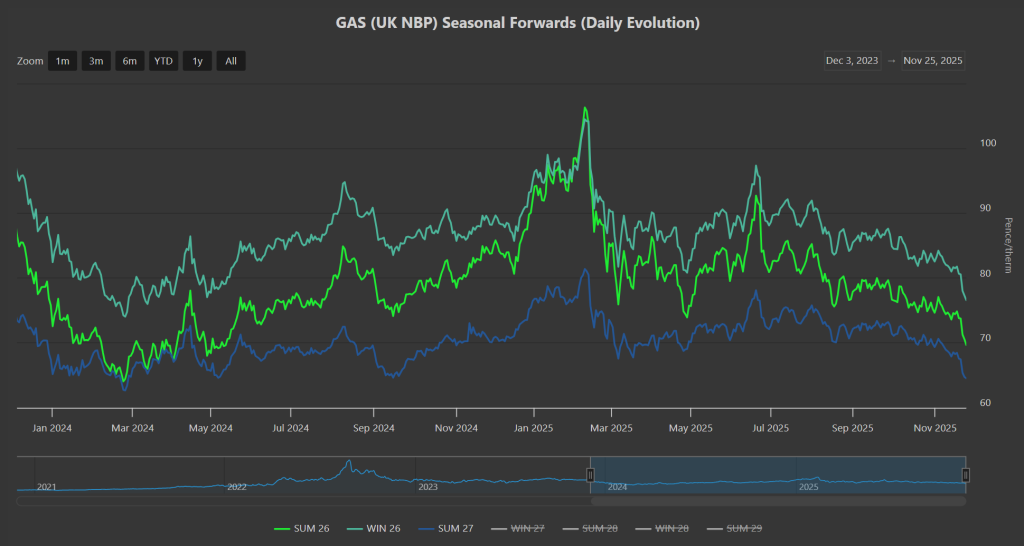

Gas markets are still giving up value almost two months into Winter-25 – please see chart below.

The front 3-Seasons are heading toward a retest of the lows we saw back on 26th Feb ’24 (following a winter of prices having fallen 30%) .

Today, prices opened lower versus yesterday’s close, though prices recovered marginally as the afternoon wore on.

Unseasonably bearish drivers include forecasts of milder weather over the coming weeks which will of course lower demand and limit storage withdrawals – despite European storage now having fallen to 78%, this is is only 6% below the 5-year average for this time of year.

LNG arrivals are strong and Norwegian pipeline flows are comfortably above their 10-day moving average – this amid (perhaps unrealistic) optimism of an end to Russia’s war on Ukraine which would lead to an even more comfortable supply outlook for Europe/the UK.

Notably, China’s 30-day moving average for LNG imports is at 207k tonnes – so down on last year (off the back of falling Industrial outputs and talk of weaker growth numbers).

Indeed, Asia’s demand remains subdued across the board – but of course, the introduction of more direct LNG supply routes to Asia from LNG Canada and Arctic 2 has Asia’s supply pretty much covered anyway, so competition for LNG from the US and Qatar is significantly mitigated (meaning Europe can afford to let gas prices fall a bit).

It’s traditional/prudent/conservative for both Fixed and Flex clients to secure prices in the summer months for winter delivery – indeed, leaving heavy percentages of gas volumes exposed to the vagaries of winter is a very risky move.

However, many Industrials will be scratching their heads at the soft landing we’re seeing at the onset of Winter-25 – will it persist?

Will we see another heating season like Winter-23 when prices dropped month-on-month (if you recall, it was the second warmest on record for England and Wales, with average temperatures 1.2°C above the 1991-2020 average)?

Well, let’s remember we’re still only in Q4, and traditionally Q1 is when prices are most subject to supportive drivers and price spikes.

But if Ukraine and Russia reach agreement, and Russian flows return in one form or another (most likely LNG given that Nordstream is in pieces on the seabed), then prices will inevitably fall off a cliff.

Monthly Day-Ahead averages for November so far are holding steady in the mid-70s, at 76p/therm (or 2.6p/kwh exc. non-gas).

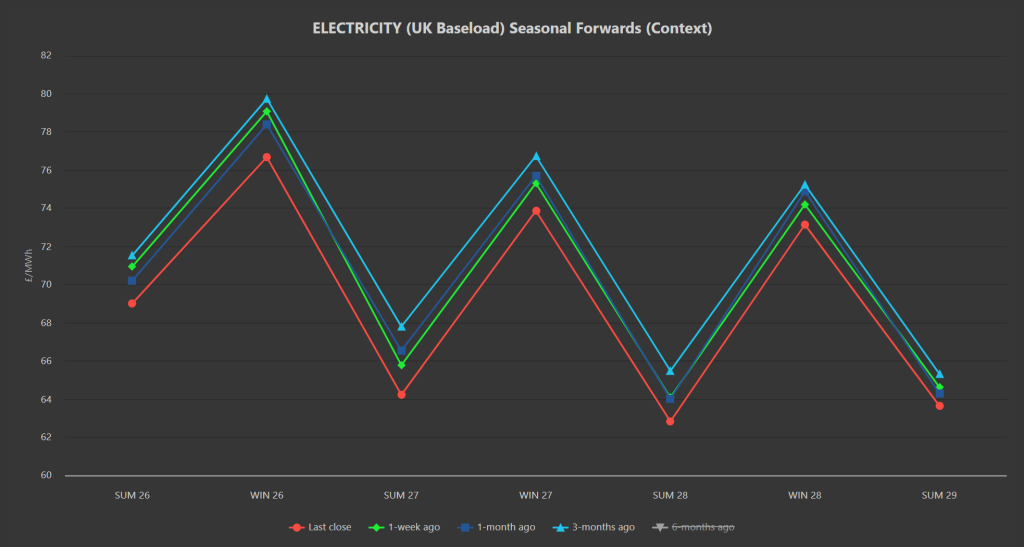

ELECTRICITY & CARBON

Electricity Seasonal Forwards all the way out are down on the week/month/3-months.

On the Carbon side of things, UKAs continue to trade below the increasingly important resistance level of £58.50/tn, but have failed to fall back (yet) to the increasingly important support level of £55.50/tn.

Instead, traders are carving out consolidation patterns between these two levels pending bullish/bearish stimulus.

Today’s UK electricity generation mix is bullish in nature given patchy wind outputs – specifically, renewables are contributing 27%, thermal at 48% (gas and coal) and low carbon at 15% (nuclear and imports).

Monthly Day-Ahead averages for November so far are at £78/mwh (or 7.8p/kwh exc. non-energy).