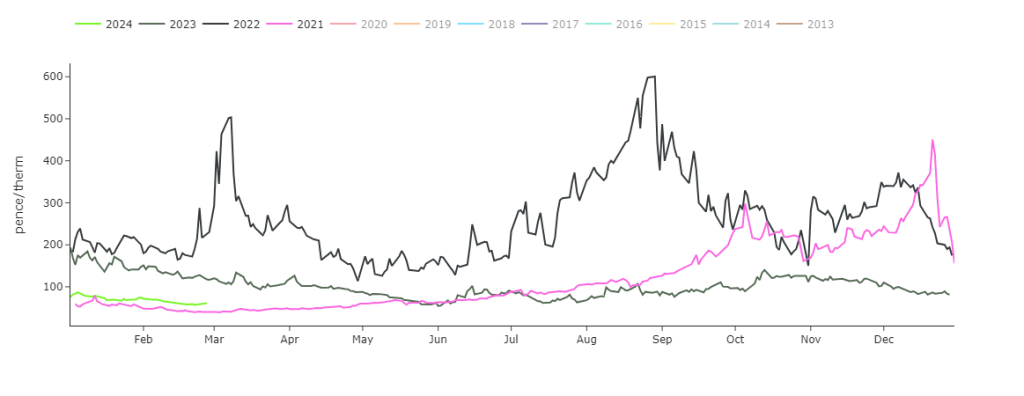

Month-Ahead delivery prices now sit circa. 33% above those printed in 2021, but 62% below 2023 and 74% below 2022 (see chart).

As predicted, UK gas prices began to retrace/correct from oversold levels this morning – supported by higher heating demand amid lower temperatures.

The UK system was short for much of the day on Tuesday (demand outstripping supply), so relied in part on storage withdrawals.

However, European storage remains at 63% fullness versus 5-year average of 50% (with only 32 days of Winter-23 remaining).

A small outage at the UKCS (Continental Shelf) lowered flow today but is expected to be short-lived.

Wind outputs are picking up and should extend into the weekend.

Russia announced a halt of petroleum products beginning March (which tallied with OPEC+ announcing they could extend supply cuts to support prices).

Not surprisingly, bullish momentum ensued with UK gas prices lifting circa. 2p/therm following the announcement.

Down the curve, contracts are trading sideways in the main.

On the supply side, Skarv gas field in Norway is undergoing unscheduled maintenance.

European LNG imports are predicted to double from 70 million tonnes per year in 2021 to around 140 million in 2030.

Increases in LNG demand are due to long-term sale and purchase agreements agreed for security of LNG (following Russia’s closure of Nordstream), as well as increased demand from China and other developing countries.

Looking at the bigger picture, only geo-political unrest poses any risk to a continuation of the prevailing long-term bear trend.

Monthly Day-Ahead averages are on target this month (so far) to achieve 63p/therm (or circa. 2.15p/kwh).

ELECTRICITY & CARBON ALLOWANCES

Looking to the continent, near-term delivery electricity prices inched down yesterday as an anticipated recovery of French nuclear availability combined with prospects of rising solar generation and milder temperatures.

After a slow bearish morning, the power curve prices posted substantial gains on Tuesday afternoon, buoyed by a steep rebound of gas and carbon prices on an extension of LNG facility outage and significant short covering in the emissions market.

Prices extended their upward correction this morning, again supported by a downward revision of temperatures and wind generation forecasts for early March.

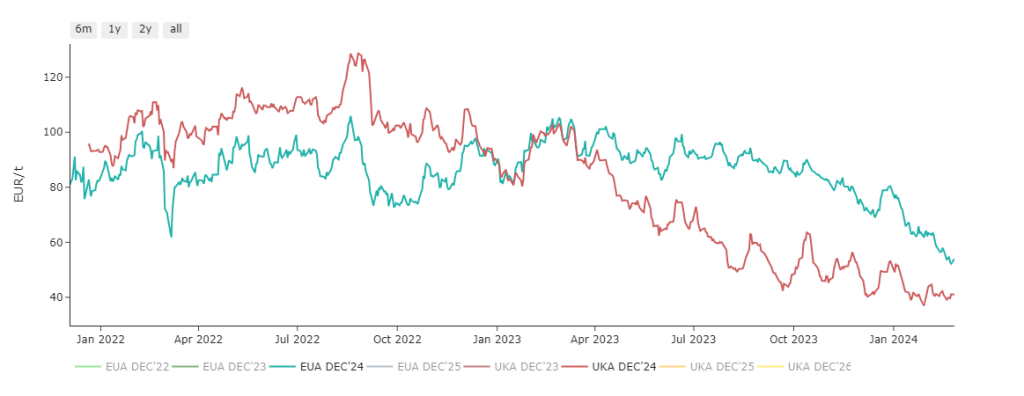

Comparing EUAs and UKAs (European carbon versus UK carbon), UKAs appear to have plateaued in and around £35 to £40/tn – whilst EUAs continue to fall, reducing the relative discount of UKAs to EUAs (see chart).

It seems likely that the counterparts are heading toward parity (following the disparity we’ve seen since UKAs launched in May 2021).

Nonetheless, keep in mind that fundamentally there is little reason for prices to go up at the moment and any rebound could turn out to be short lived.

Back in the UK, our electricity generation mix bearish in nature with renewables contributing 43% and gas-for-power burn at 31%.

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £59/mwh (or 5.9p/kwh).