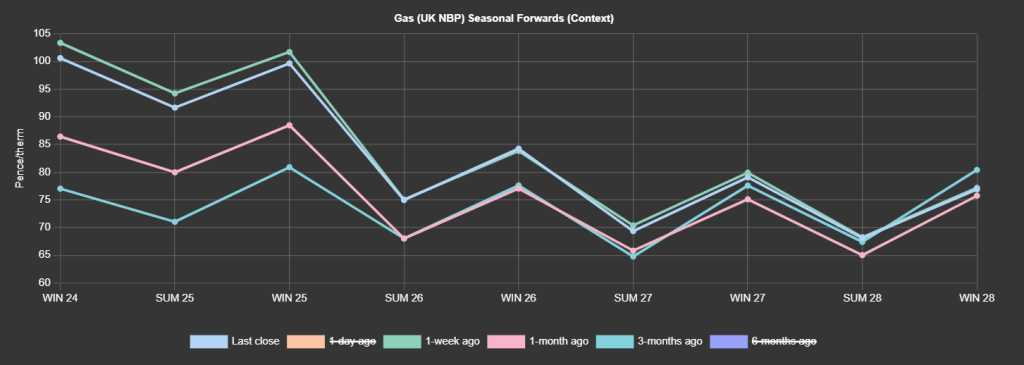

Seasonal Forwards are down on the week, but up on the month/3-months ago (see chart).

Prices are trading sideways today having moved lower yesterday.

The UK gas (NBP) curve traded lower off the back of weaker demand, comfortable supply and some likely profit taking.

Prices might have traded lower but for news released mid-afternoon detailing production reductions at Teesside of circa. 5mcm/d until 3rd July.

Whilst demand is down, on the supply side, lower LNG delivery to Europe (with more cargoes heading to Asia) is an increasingly supportive driver.

LNG send out is a concern with only one arrival expected in early June.

Fundamentally speaking, as a consequence to Russia’s lost gas flows, Europe can no longer do without LNG (and it must therefore compete with Asia).

Indeed, LNG continues to increase its share in the European energy mix.

While Germany continues to expand its fleet of floating LNG import terminals (by bringing it to six at the end of this year), other European countries are finding ways to import LNG.

For example, Hungary is one of the few European countries that still imports Russian gas but is also looking to source elsewhere.

Algeria’s Sonatrach said yesterday that part of a cargo of LNG delivered into Croatia’s floating LNG terminal this month would be used to supply Hungary (after regasification, the gas will be transported through the Croatian gas network).

Back in the UK, CCGT demand (gas-for-power burn) has thankfully dropped off with wind outputs rising into the weekend.

Today’s outlook is one of rangebound price action – with perhaps some chance of a slight d-o-d increase after two consecutive down days to start the week.

On the bearish side, LDZ demand (heating demand) is flat then falling over the weekend and into next week.

Overall, with better wind outputs and reduced thermal generation (gas-for-power), our balance remains comfortable and loose with storage injections required to balance the system.

On the bullish side, on top of weak LNG dynamics, outages and unscheduled extensions pose a risk as well as reactions to news driven geopolitical events.

The OMV issue, whilst unresolved, will remain supportive (with the likely outcome being Gazprom ceasing to deliver gas to Austria).

Norwegian flows to UK and NW Europe remain above the 5-day moving average, notwithstanding reduced capacity due to maintenance.

Consensus remains that Europe is on track to achieve 100% storage levels by Winter-24 (early Oct ’24).

Monthly Day-Ahead averages are on target this month to achieve 75p/therm (or circa. 2.5p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, near-term delivery prices continued to ease yesterday off the back of forecasts of improved wind outputs for today.

EDF stopped its Paluel 3 (1.3GW) nuclear unit due to a fire in the main transformer of the reactor.

The outage is set to last around a month (although similar fire at the Chinon nuclear power plant in Feb ’24 kept Chinon 3 offline for around eight weeks…)

Day-ahead prices could be supported today off the back of subsequent weakening French nuclear generation.

On the regulation side, French president Emmanuel Macron proposed the head of the nation’s nuclear waste agency (ANDRA) to lead the ASN nuclear safety authority.

If approved by parliament, Pierre-Marie Abadie first tasks will be to oversee the merging of the ASN and IRSN.

The emissions and power curve prices noticeably declined yesterday, dragged down by a retracement of gas prices although the move seemed driven more by technicals than fundamentals (profit-taking/repositioning).

Markets feel directionless at the moment (as evidenced by this morning’s rebound from Tuesday’s bearish session) – torn between bearish short-term fundamentals and supportive risks of supply reduction.

European emissions prices (EUAs) dropped below the psychologically important 1-year moving average on Tuesday.

Still strongly correlated to the gas market, the EUA Dec’ 24 benchmark closed the day at 74.58€/t, -1.67€/t from Monday.

Market participants are likely waiting for the COT (Commitment of Traders report) due out today detailing the evolution of speculators’ positions following last week’s sharp rises i.e., has there been a marked trend reversal?

Back in the UK, UKAs (UK Allowances) are still taking a breather – now trading at circa. £45/tn (Dec-24 benchmark) – having broken above the highs printed on 25th Mar ’24 and having breached overhanging resistance trendlines.

Our electricity generation mix is bearish in nature today with renewables contributing 39%, thermal at 16% (gas and coal) and low carbon at 24% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £72/mwh (or 7.2p/kwh excluding non-energy).