Nearly a month into Winter-25, markets remain soft off the back of benign fundamentals and low demand.

The heating season is nearly upon us (early November) – so expect prices reacting to increasing demand and increased storage withdrawals over the coming weeks.

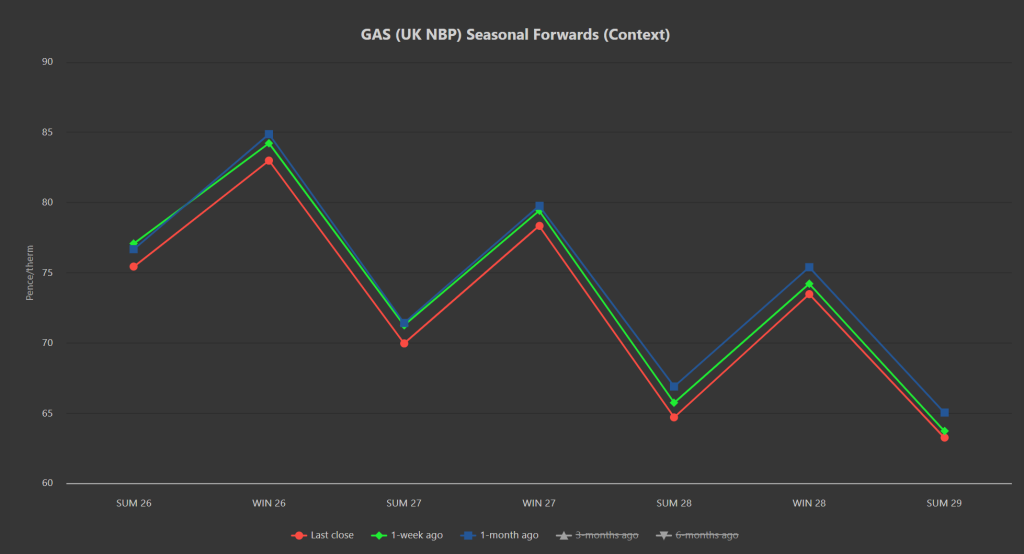

As per the chart below, Seasonal Forwards are down versus 1-week/1-month ago – this late bearish inclination can be attributed to a better supply outlook than was anticipated (by the doomsayers throughout the summer months), and a better European storage fullness than was feared (currently 83% versus the 5-year average of 89%).

We’re starting to see an increase in net withdrawal days (as opposed to net injection) as the storage charts begin to plateau, before likely rolling over into constant withdrawal beginning mid-November, lasting until mid-March.

On the geopolitical front, markets have learnt not to react too quickly to Trump’s vacillating strategies, which explains why market participants have shrugged off the potential impacts of Israeli strikes on Gaza overnight (threatening the ceasefire).

The much hyped Hurricane Melissa has also had little impact on prices despite the widespread chaos she’s left in her wake,

Monthly Day-Ahead averages for October remain at 78p/therm (or 2.66p/kwh exc. non-gas).

ELECTRICITY & CARBON

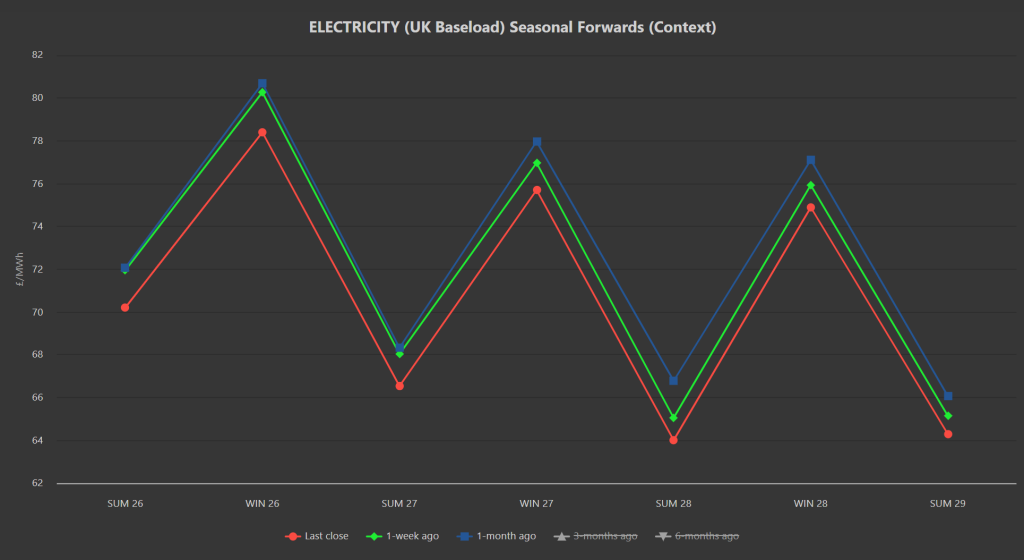

Electricity prices continue to mirror the low volatility of gas markets – as per the chart below, Seasonal Forwards are down versus 1-week/1-month ago.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are bracketing in a triangle/consolidation pattern (please see chart below).

At the time of writing, prices are holding steady in the mid-50s (currently at £55/tn) – having failed to break out of the triangle to the downside earlier this week (with prices still in the triangle, now heading to retest the upper extremity of the consolidation pattern).

The secondary market remains at a discount to auction settlement prices – reflecting increased speculative interest in emissions auctions as winter deepens.

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 40%, thermal at 24% (gas and coal) and low carbon at 18% (nuclear and imports).

Monthly Day-Ahead averages for October so far are at £71/mwh (or 7.1p/kwh exc. non-energy).