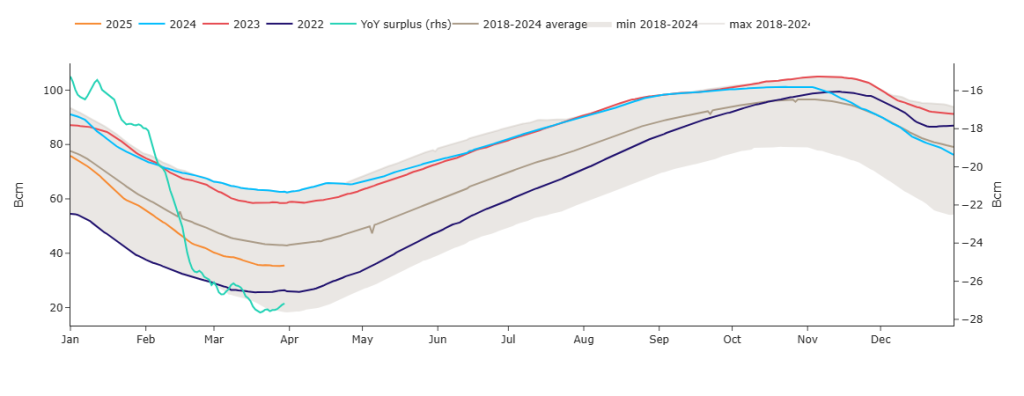

As of yesterday, the Summer-25 delivery period has begun, and so all eyes are now trained on storage levels (please see chart below detailing prevailing % fullness versus recent years, and the y-o-y deficit).

It’s customary for traders to buy gas during the summer months (when it’s traditionally cheaper), then put it into storage with a view to selling the gas during the winter months for a nice profit when demand (and value) is highest.

However, this year is different, prevailing monthly Forward summer prices are only marginally below those for Winter-25 delivery – making for a less profitable summer-winter spread.

So, as things stand, traders have less incentive to stockpile gas volumes for Winter-25 delivery (pending the spread widening as summer conditioning deepens).

As such, we’ll be keeping a close eye on how quickly gas is injected into European storage over the coming weeks/months (in time for the mandated 90% fullness requirement come 1st Nov).

Even though this summer’s Norwegian gas maintenance schedule is forecast to be lighter than it’s been over the past few years, any drop in flows will likely be a supportive price driver.

As can be said for increased competition for LNG with Asia, or unexpected cold spells limiting our ability to inject into storage.

On the other hand, market bears still cling onto the hope that Russian flows may yet still be reintroduced into the European system (subject to a deal being reached over the Ukraine/Russia conflict).

Though increasingly, given Putin’s (not surprising) reluctance to play ball (rejecting Washington’s initial proposal, then adding conditions to a Black Sea ceasefire) it looks more likely that Trump’s frustration will lead to further sanctions on Russian oil.

So, in the absence of additional pipeline flows from Russia, Europe/the UK will need to hope that Norwegian scheduled maintenance is kept short and Asia doesn’t compete too hard for LNG cargoes.

Trump’s tariffs are rumoured to be already negatively impacting China’s economy off the back of slowing growth and a property sector in turmoil – as such, Chinese demand is unlikely to spike over the summer months.

Having said that, Trump is expected to announce additional wide ranging tariffs today across multiple trading partners (including the UK) – so we should probably start to factor-in slowing economic growth and demand for fuels globally (not just in China).

Less demand over the coming months against a backdrop of summer conditioning will, of course, soften prices – but if economies are retracting, will anybody benefit?

In the near-term, temperatures are expected to drop-off next week so storage withdrawals will remain under pressure into the second week of the month.

Monthly Day-Ahead averages for March closed out at 101p/therm (or approx. 3.46p/kwh excluding non-gas).

It’s early days, but this month’s Day-Ahead averages are at 105p/therm (or approx. 3.6p/kwh excluding non-gas).

ELECTRICITY & CARBON

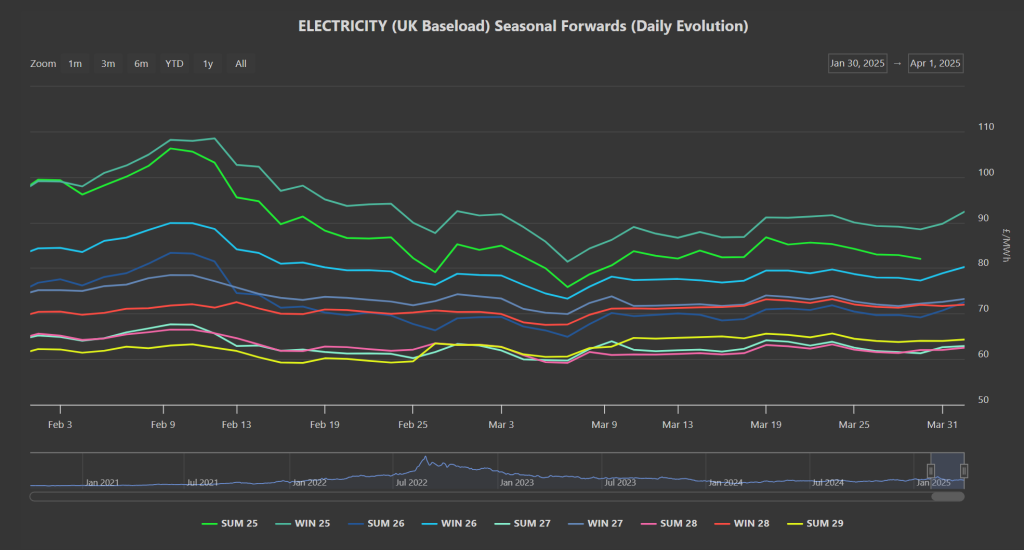

Summer-25 closed out at £98.78/mwh (when trading for this season ended last week).

Looking up and down the curve, Summer-29 delivery is at a 33% discount versus the most expensive season (Winter-25) – please see chart below.

Today’s UK electricity generation mix is very bearish in nature, with renewables contributing 70%, thermal at 5% (gas and coal) and low carbon at 16% (nuclear and imports).

On the Carbon markets, UKAs (UK mandatory allowances for heavy emitters) have repeatedly rejected (to the downside) the upper extremity of a bearish trend channel first formed back on 10th Feb.

UKA mid-price is now consolidating in a tight range (£44/tn to £47/tn) with investment funds still net long (or in a ‘buy’ position).

Electricity Monthly Day-Ahead averages last month closed out at £89/mwh (or approx. 8.9p/kwh excluding non-energy).

So far this month, Day-Ahead averages are on target to achieve £78/mwh (or approx. 7.8p/kwh excluding non-energy).