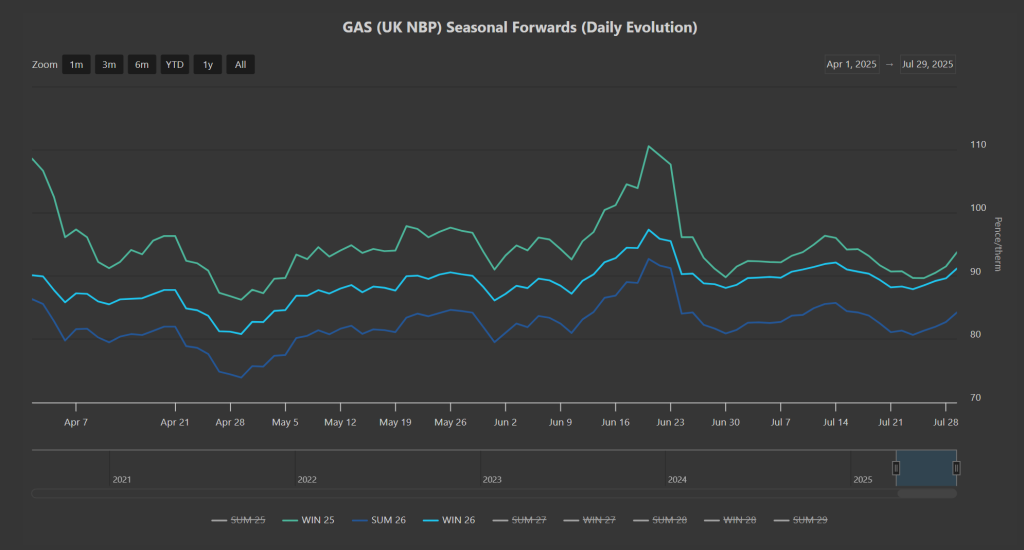

Since Summer-25 began on 1st Apr, Winter-25 delivery prices have traded within a 20% range – please see chart below.

At the time of writing, we’ve failed to break below the most recent Winter-25 lows of 89p/therm (posted on 30th Jun), and prices now look set to retest the most recent high of 96p/therm (posted on 11th Jul).

Since 24th Jun, Winter-25 prices have only traded with a 7% range – so, it’s safe to say that key market drivers have been balanced.

Reasons for the marginally bullish start to the week include Trump’s ramped-up pressure on Russia to make peace with Ukraine (by threatening more far-reaching economic sanctions that will in turn reduce Europe’s gas imports); rumours of increased Houthi activity in the Red Sea (threatening LNG transit); an earthquake measuring 8.8 on the Richter scale off the coast of Russia putting much of the Pacific region on high alert of Tsunamis (Japanese Nuclear faculties have been suspended for the time being, increasing that region’s reliance on gas-for-power burn); trading floors are quiet given the summer holiday season (so liquidity is poor and bid/offer spreads are wider than usual); disappointing wind outputs (increasing storage withdrawal and gas-for-power burn).

So, until further notice, we’re on an uptick – as such, Industrials that have yet to hedge Winter-25 delivery may wish to sit tight pending the next dip (given that we’ve still got the whole of August to go until we hit the ‘shoulder-month’ – September).

In other price-supportive news, LNG Canada (which started operations at the end of June) has reported technical problems as it ramps up production.

Front-month Asia JKM prices have increased more moderately than their European counterparts (widening the Asian discount – so LNG vessels continue to head toward European ports to maximise profits).

The ever-important European storage fullness is at 68% versus the 5-year average of 75% – so closing-in on the mandated 80% in time for the heating season (which starts in earnest around November).

Monthly Day-Ahead averages for the month so far have spent the last two weeks at 81p/therm (or approx 2.7p/kwh excluding non-gas) – a reflection of very flat near-term risk.

ELECTRICITY & CARBON

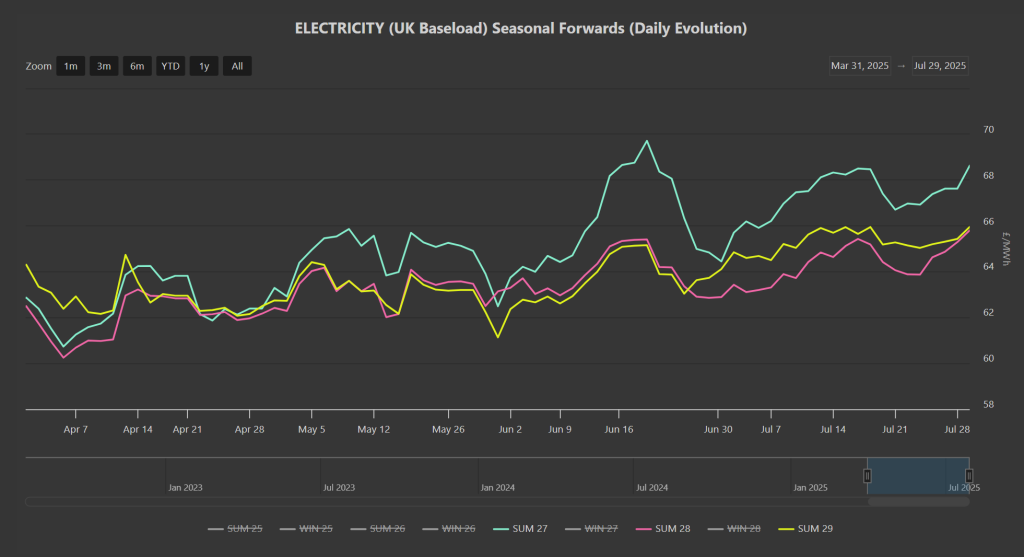

Notably, Summer-27/Summer-28/Summer-29 remain below £70/mwh, but continue to increase in value as the summer progresses (and winter grows ever nearer) – please see chart below.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are at £51.93/tn on the mid-price (and look set to retest upside resistance at £53/tn where bearish and bullish trend channels intersect).

Today’s UK electricity generation mix is neutral in nature – specifically, renewables are contributing 32%, thermal at 23% (gas and coal) and low carbon at 35% (nuclear and imports).

Monthly Day-Ahead averages for the month so far have spent the last week or so at £79/mwh (or approx 7.9p/kwh excluding non-energy) – a reflection of very flat near-term risk.