Bulls picked up this morning where they left off yesterday afternoon.

At this morning’s bell, prices gapped up to open above last nights close.

So what’s driving this bullish momentum (given that prevailing drivers are so benign i.e., high storage/favourable weather conditions/solid supply dynamics)?

Well, the UK system opened short again this morning making it a third day in a row where demand has outsripped supply.

In the absence of sustained appetite to take the market even lower, market participants will often look for a reason to test upwards resistance.

As such, LNG could be blamed for the upwards move following closure of Train 3 at Freeport, Texas and Presidents Biden’s pausing of new LNG projects.

LNG vessels are also enduring voyage delays with shipping companies opting to reroute around the Cape of Good Hope to circumvent the Red Sea (following another attack over the weekend which caused a tanker blaze).

Also, we’ve seen some flip-flopping on weather forecasts for late February – which is now expected to bring below than average seasonal temperatures.

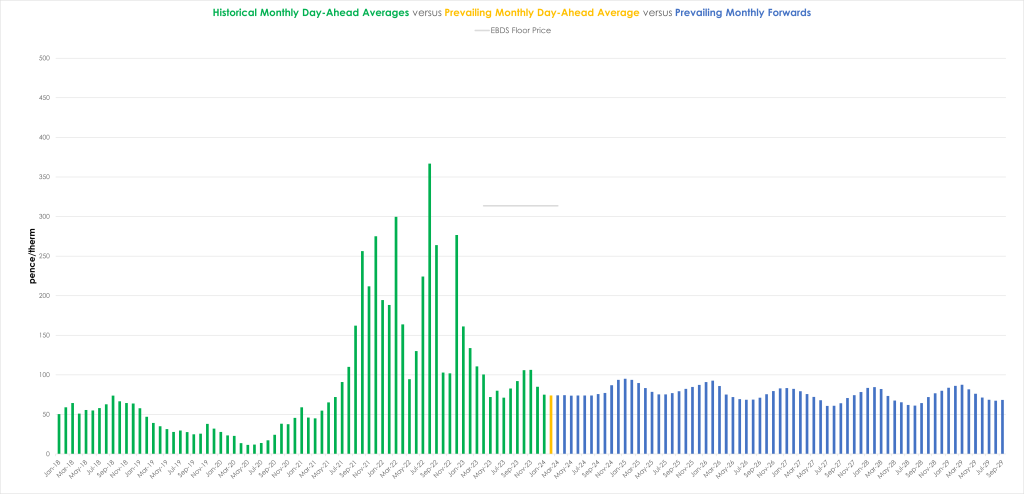

Monthly Day-Ahead averages achieved 75p/therm (or 2.5p/kwh) for Jan ’24.

ELECTRICITY

Looking to the continent, near-term delivery prices fell yesterday thanks to revised forecasts of even warmer temperatures and improved wind generation until the end of next week.

NW Europe is likely to experience stable westerly flows, providing consistent baseload power which is forecasted to peak around Sunday/Monday.

We may even see negative intraday prices in Germany over the coming weekend.

Back in the UK, our generation mix at the time of writing is very bearish with 49% renewables and only 25% gas-for-power burn.

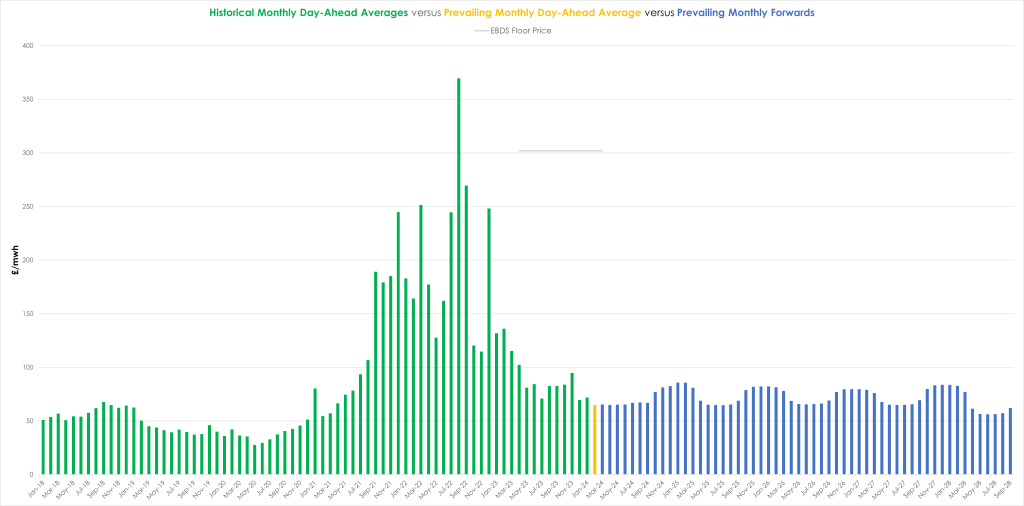

UK electricity monthly Day-Ahead averages achieved £72/mwh (or 7.2p/kwh) for Jan ’24.