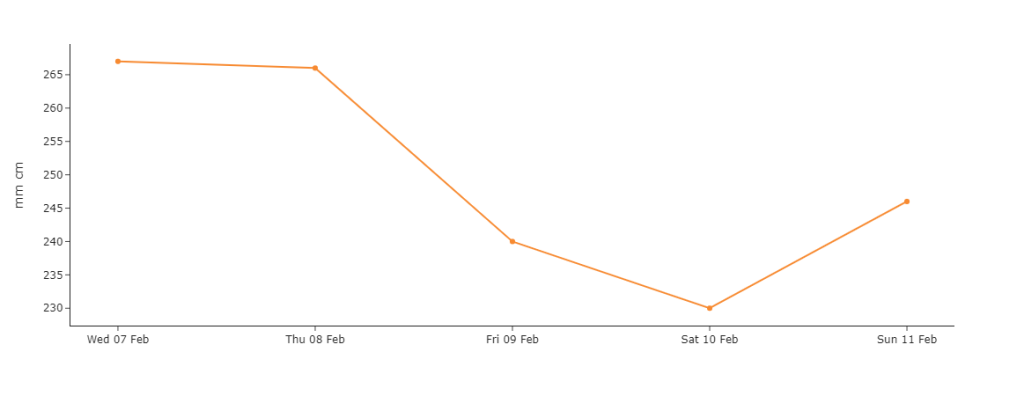

UK gas demand is expected to fall over the coming days (see 5-day chart).

The UK system was only very marginally short at this morning’s open (demand outstripping supply) – in the main, supply/demand remains well-balanced with Norwegian and UKCS (Continental Shelf) flows back on the rise following the resolution of unscheduled outages at Troll (Norway) and Barrow (Cumbria), and LNG arrivals in good shape.

It’s been another day of neutral to bearish price action, with contracts all the way down the curve drifting marginally lower.

Prices remain soft off the back of wet and windy forecasts for most of February.

Whilst drivers are mostly bearish, prices remain supported at prospects of a colder spell toward the end of the month and of course geopolitical risk across the Middle East/Ukraine.

Despite recent withdrawals, European gas inventories remain at historically high levels (69% versus 5-year average of 57%).

Will we make it to the end of Winter-23 with more than 50% left in the tank?

Probably not, but reserves will still be very high for the time of year.

Monthly Day-Ahead averages are on target this month (so far) to achieve 70p/therm (or circa. 2.4p/kwh).

ELECTRICITY & CARBON ALLOWANCES

Looking to the continent, European near-term delivery prices rose marginally yesterday buoyed by expectations of a sudden decline in wind outputs and downward revisions of short-term temperature forecasts.

However, any bullish momentum was offset by multiple French nuclear reactors coming back online following outages.

Down the curve, prices finished the day marginally up mirroring gains in the gas and carbon market against a backdrop of balanced fundamentals.

Plentiful storage and persistent demand destruction are keeping a lid on any meaningful upside.

Given balanced key drivers, weather outlooks remain an obsession for market participants – so any flip-flop is causing prices to retest areas of support/resistance in what is essentially a tight rangebound market with Summer-24 now clearly on the horizon.

Only modest moves on the carbon markets – the main news yesterday was on the regulation side with the European Commission proposing an ambitious 90% greenhouse gas emission reduction target by 2040 and net-zero by mid-century.

The announcement is having little impact on European/UK emissions prices today as its impact is outside the market horizon (while the level proposed is in line with most expectations anyway).

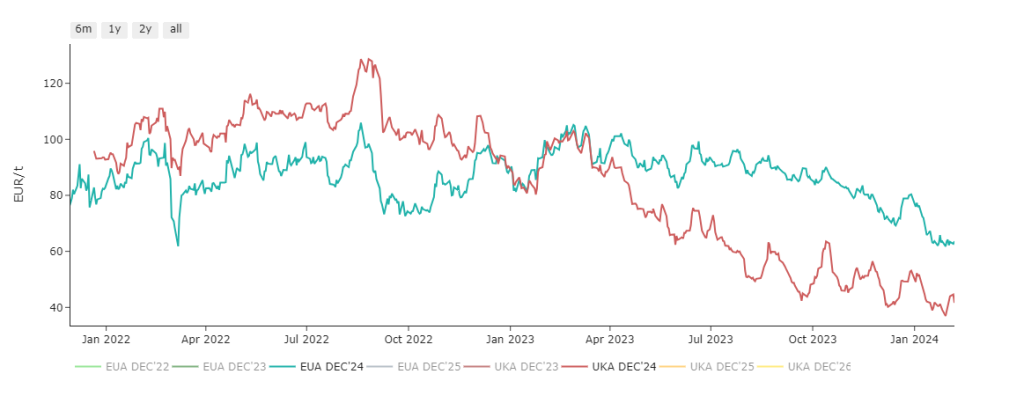

UKAs (UK mandatory carbon allowances) remain at a significant discount to its European counterpart (EUAs) – see chart.

Our generation mix today is back to bullish – only 15% renewables versus 54% gas-for-power burn.

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £54/mwh (or 5.4p/kwh).