Back on the morning of 26th June, we issued blanket emails to FLEX clients (with near-term open volumes) detailing that markets were in a pronounced dip (against the backdrop of a shaky 60-day ceasefire agreement).

We pointed out that, all variables considered, we thought it prudent that clients thought seriously about closing out not just the front month, but the whole of Q326 whilst the going was good.

Thereafter, over the following days, liquidity dropped but thankfully the large majority of Q3 Positions were filled.

As of last night, diplomacy has once again collapsed, and hostilities across the piece have resumed.

For their part, Iran seems unwilling to allow free and safe transit through the Strait’s international waters (and is attacking ships accordingly).

On the US side, the Trump Administration’s maximalist demands will never be accepted by the other side (and so negotiations are going nowhere).

This morning, markets opened higher across the globe as the US launched fresh airstrikes on 80 military targets across Iran in response to the regime attacking a Qatari LNG tanker trying to cross the Strait.

The US has also pulled Iran’s oil export waiver (which formed part of the Iranian benefits of the MoU).

By way of further retaliation, the Revolutionary Guard (the IRGC) launched missiles at 85 US military installations across the Middle East.

Not surprisingly, Brent crude is back up to $78/barrel amid renewed fears over supply tightness.

Tightness is also being felt again across gas markest given the slow pace of Europe’s storage replenishment so far this summer – fullness to date is at 51% versus the 5-year average of 62%.

As for next steps, Trump is being quoted as stating an interim agreement to end the war with Iran was “over”.

When asked before the NATO summit in Turkey whether the memorandum of understanding was broken, Trump said: “It’s a very interesting question. To me, I think it’s over. I don’t want to deal with them. They’re scum. They’re sick people. They’re led by sick people, as far as I’m concerned, it’s just a waste of time dealing with them.”

A top Iranian negotiator, parliament speaker Mohammad Baqer Qalibaf, has accused the US of breaching the ceasefire agreement, citing not only the latest military strikes, but renewed oil sanctions, violations of Iranian “adjustments” in the Strait of Hormuz, and Israeli attacks against Lebanon.

On a post on X, Qualibaf has stated, “the era of bullying and extortion is over, we don’t fold.”

Specifically, Iranian media is reporting explosions on Kharg Island, on Qeshm Island and in the southern port cities of Sirik and Bandar Abbas – so, evidently, the US is targeting the regime’s primary sources of export revenues, oil.

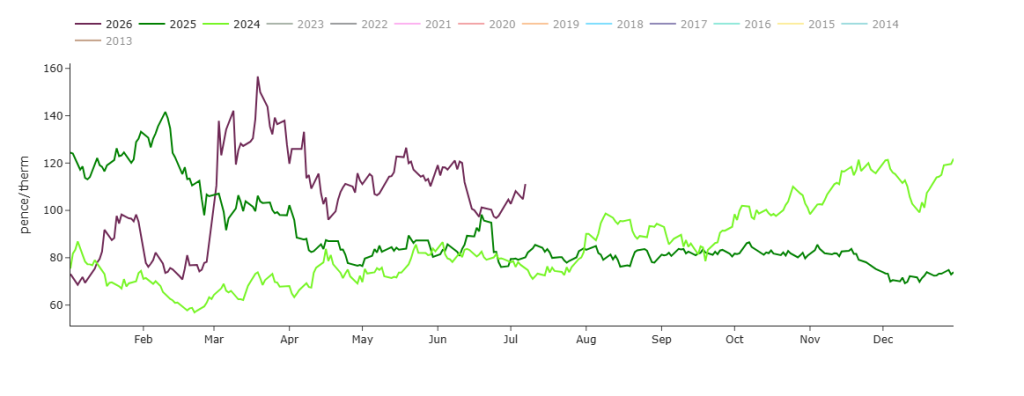

Monthly Day-Ahead Averages for July so far are at 107 p/therm (or 3.65 p/kwh exc. non-gas).

The chart below details the evolution of Month-Ahead prices for ’24/’25 and ’26 so far.

As you can see, until yesterday’s flare up, Month-Ahead prices were set to fall below ’25 prices this time last year.

On the FLEX side of things, for clients with remaining near-term open volumes, we’ll look to advise on potential intraday dips and hedging opportunities over the coming days – at the time of writing, prices are softening compared to the bullish volatility we saw at this morning’s open.

ELECTRICITY & CARBON

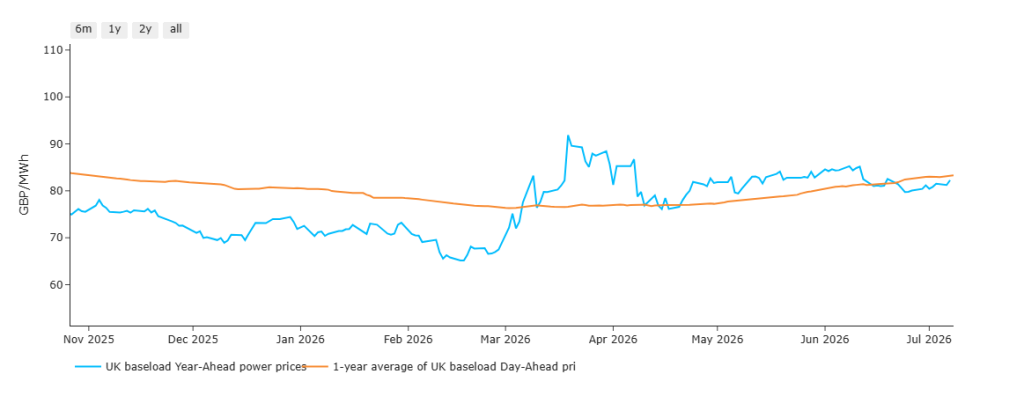

The chart below details UK electricity Year-Ahead prices versus the 1-Year Average of Day-Ahead prices since late-Feb.

By way of explantion, when the blue line is above the orange line, mid-term delivery prices are at a premium to an average of the last 12 months.

Prior to the onset of the US/Israeli offensive, prices were enjoying a soft-landing heading into Summer-26 – thereafter, Year-Ahead has remained consistently at a premium despite the otherwise ‘summery’ conditions.

For the week beginning 22nd Jun ’26, the blue line fell back below the orange line indicating that prices were in a dip versus wider context (hence our Q3 hedging recommendations on 26th Jun ’26).

At last night’s close, the chart still indicates good prevailing value – however, we expect this to be tested at today’s close, and for the rest of the week.

On the Carbon side of things, Dec-26 UKA delivery is directionless at £56.31/tn (and the spot is at mid 55s).

Monthly Day-Ahead Averages for July so far are at £83/mwh (or 8.3 p/kwh exc. non-energy).

On the FLEX side of things, for clients with remaining near-term open volumes, we’ll look to advise on potential intraday dips and hedging opportunities over the coming days – at the time of writing, prices are softening compared to the bullish volatility we saw at this morning’s open.