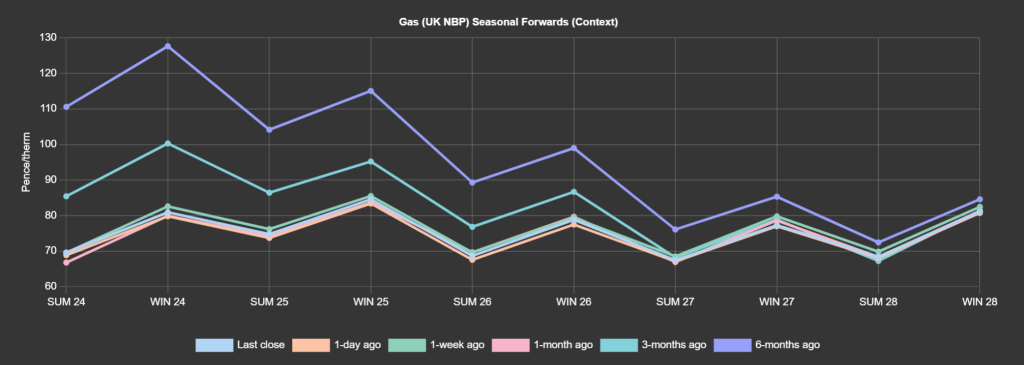

It’s been a week of sideways price action, though prices down the Seasonal curve finished marginally down on the week (see chart).

Recent bearish action reflects inevitable summer conditioning, with above seasonal temperatures and strong winds as key drivers.

Temperature forecasts are above seasonal norms until late next week.

In the face of overwhelmingly bearish drivers (high storage, low demand, solid supply, high temperatures, solid renewables outputs), risk still persists as geopolitical tensions rise – increasingly between Iran and Israel.

Escalations are likely to give rise to fears over supply tightness/disruption.

For the time being, markets have found equilibrium – with very little conviction from bears or bulls.

Noise aside, and in the absence of further geopolitical turmoil, it’s likely we’ll see improved value for Winter-24 delivery as the summer progresses.

Monthly Day-Ahead averages are on target this month to achieve 63p/therm (or 2.15p/kwh).

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices were soft throughout the week amid very mild temperatures, strong renewables outputs and long nuclear production (supplying more than demand required).

With temperatures set to peak over this weekend (coinciding with traditionally lower demand on weekends), and with both wind and solar generation expected to increase, it appears inevitable that negative prices will print today or tomorrow.

On the carbon markets, prices moderately rebounded on Thursday, driven primarily by marginally firmer gas prices despite unchanged and still mostly bearish fundamentals.

Market participants showed barely any response to the 2023 verified emissions report and the COT (Commitment of Traders report), as both aligned with expectations and impacts were already priced-in.

The latter revealed a further reduction in speculators’ net short position – though this reduction was less pronounced compared to previous weeks – likely indicating that speculators may be content with their current position and potentially prepared to reinstate shorts if the grim outlook for the industrial sector persists longer than anticipated.

Dec-24 contracts for UKAs finished down on the week at circa. £35/tn.

Our electricity generation mix is very bearish in nature today with renewables contributing 70%, thermal at 6% (gas and coal) and low carbon at 20% (nuclear and imports).

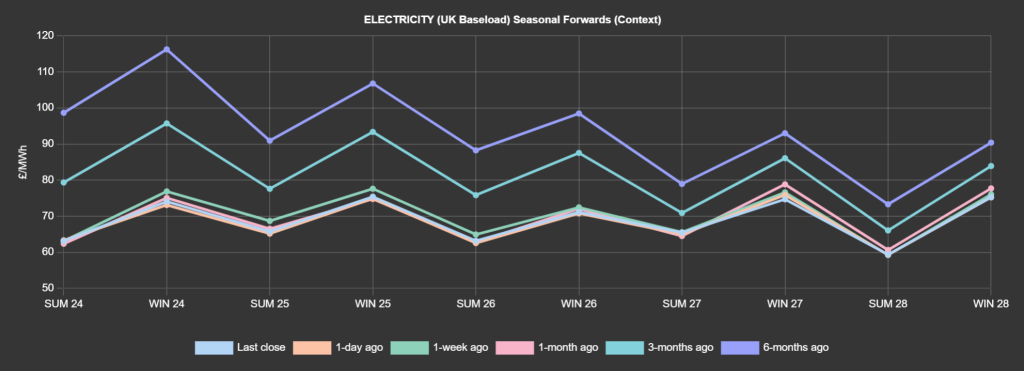

Monthly Day-Ahead averages are on target this month to achieve £57/mwh (or 5.7p/kwh).